US and Israeli strikes on Iran, followed by Iranian retaliation, sharply escalated security risks in the Middle East in March. The United States is seeking regime change in Iran as well as the permanent dismantling of the country’s nuclear and missile programmes. From a market perspective, the key issue is the Strait of Hormuz, through which roughly one fifth of global oil and liquefied natural gas flows. The disruption of tanker traffic in the Strait led to a sharp rise in oil prices, adding to inflationary pressures.

The most significant economic risk relates to how long the Strait of Hormuz remains closed. Most assessments suggest the conflict will ultimately end in a negotiated settlement, but a prolonged crisis would cause substantial damage to the global economy—particularly for energy‑importing countries and Europe. The United States has demanded that the strait be reopened and is currently deploying additional military assets to the region.

Market impact so far has been contained

Overall, the impact of the war involving Iran on global equity markets has so far been relatively modest, even though the sharp increase in oil prices has raised the risk of stagflation. The MSCI World Index has fallen by around seven per cent from its February peak and by roughly four per cent since the turn of the year.

Historically, the market effects of many military conflicts have been short‑lived. Both the Gulf War in 1990 and the Iraq War in 2003 lasted around six months. In 1990, crude oil prices peaked in late September and early October, when the US began planning military operations. Equity markets rebounded in January 1991 as the offensive commenced. Iran may prove a more challenging adversary for the US, but the military superiority of the US and Israel is clear. That said, domestic political considerations in the US could still influence the course of events.

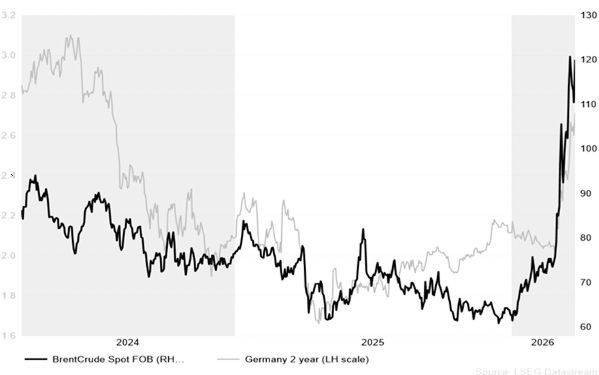

Sharp rise in interest rates

The rise in interest rates reflects renewed inflation fears, and central banks are keen to avoid repeating the mistake made after the pandemic‑era inflation surge, when rates were raised aggressively to rein in price pressures. At this stage, however, it is still too early to assess the duration of the crisis or the path of oil prices—let alone their full impact on consumers.

If the crisis remains short‑lived (lasting weeks or at most a few months), the effects on the economic outlook are likely to remain limited, and no additional monetary tightening would be required.

If the crisis drags on, consumer and corporate behaviour will be decisive. Should consumption remain resilient and continue to fuel price increases—potentially leading to renewed wage pressures—central banks may be forced to step on the brakes. Conversely, if precautionary saving increases, consumption slows, and companies postpone investment decisions, tighter monetary policy would risk deepening an economic downturn.

Diverging economic signals challenge central banks

The US Federal Reserve left its policy rate unchanged in March, and market expectations of rate cuts have faded. The US economic picture remains mixed. The services sector and consumer spending are still relatively robust, but there are intermittent signs of weakening in the labour market, with unemployment having risen to 4.4%. Consumer and producer price inflation eased somewhat, but elevated energy and services prices are keeping headline inflation above levels that would be comfortable for the Fed.

In the euro area, business surveys point to weakening activity, particularly in the services sector. Consumer confidence fell sharply in March. While baseline forecasts suggest inflation will fall below target over the longer term, an energy‑driven price shock could force the European Central Bank to consider rate hikes. In its communications, the ECB stressed that any potential fiscal support measures should be temporary and well targeted to prevent inflationary pressures from becoming entrenched. The ECB’s increasingly hawkish tone has shifted market expectations, with monetary tightening now anticipated as early as the April meeting on 30 April.

Figure: Interest rates responded strongly to the rise in crude oil prices