Despite the rhetoric, the Iran conflict has developed in a better direction. Preferences are revealed through choices—ceasefire and blockade vs warfare—as opposed to doomsday tweets and “truths”.

Conceptually, the US–Iran conflict is best understood as a bargaining problem in which bombing, blockades, and other military actions are means of applying negotiation pressure. Iran, in turn, had to close the Strait of Hormuz to restore its lost credibility and deterrence. An unforeseen problem with closing the Strait, however, is that it may drive Gulf states to invest in pipelines circumventing the Strait. If they choose to do so, Iran will be deprived of deterrence. One substitute for deterrence would be for Iran to develope nuclear weapons—the very thing that the US and Israel seek to prevent.

Continuation of bargaining through other means

Despite the fiery rhetoric, the Iran conflict has continued to develop in a positive direction, with negotiations and a maritime blockade taking over from warfare. When following the war, it is best to derive intention from actions on the ground rather than from broadcasts partially aimed at domestic audiences. This is also known in economics as the revealed preference theorem, or more colloquially, as talk is cheap.

It is too early to say whether the conflict will end in a formal peace agreement or a frozen conflict resembling the pre-war, but from an economic and market perspective, all that matters is if oil flow is restored through the Hormuz Straits.

Recent de-escalation and the incentives of both the US and Iran mean that the most likely outcome is that oil flow will be restored before the global economy suffers critical damage. This likely means higher inflation, but limited impact on economic growth and stock market earnings. Europe and other energy-importing economies will suffer more than energy exporters such as the United States. There is, of course, a significant risk that negotiations fail despite aligned incentives and that the conflict is prolonged. History is replete with conflicts that ground on despite both parties wishing to settle, such as the eight-year Iran–Iraq war of the 1980s.

Conceptually, the US–Iran conflict is best understood as a bargaining problem that began with talks in February which ran aground, escalated into open warfare, and has now de-escalated back into talks and a naval blockade. The US sought to improve its negotiating position through bombing, with the timing of the opening strikes chosen opportunistically to eliminate Iran's leadership.

Markets as a constraint on power

US President Donald Trump's foreign policy involves zero-sum bargaining with allies and adversaries alike, using maximum pressure—a type of foreign policy that naturally lends itself to economic risks and, hence, equity market turmoil. Examples of his foreign-policy misadventures include the 2017 North Korea crisis, the 2018 trade war, the recent 2025 trade war, and the current Iran war.

There is an irony in the fact that the architect of such disruptive foreign policy is himself particularly allergic to equity corrections. The combination of the policy and its architect results in reflexivity—a foreign policy that unwinds itself. The destructive foreign policy triggers a market decline; the decline unsettles the architect, ultimately leading him to back off the policy. The reflexivity is not complete, and policy ends up being partially enforced. The US has instituted tariffs on both trade wars, for example. Markets act as a constraint on power, much like institutions have done in the past. It’s fortunate that the world economy is a market economy; a command economy would not necessarily produce comparable reflexivity.

In the case of the Iran war, Trump is more sensitive to market gyrations than usual, because the US midterm elections are held on November 3. The cost of living is the dominant theme of the midterms, and a bout of oil price-driven inflation will be felt at the ballot box. This time, elevated prices cannot be blamed on President Joe Biden. In addition to their inflationary effects, wars are themselves unpopular with the US electorate—a fact that Trump is cognizant of, as he campaigned on ending the forever wars of his predecessors.

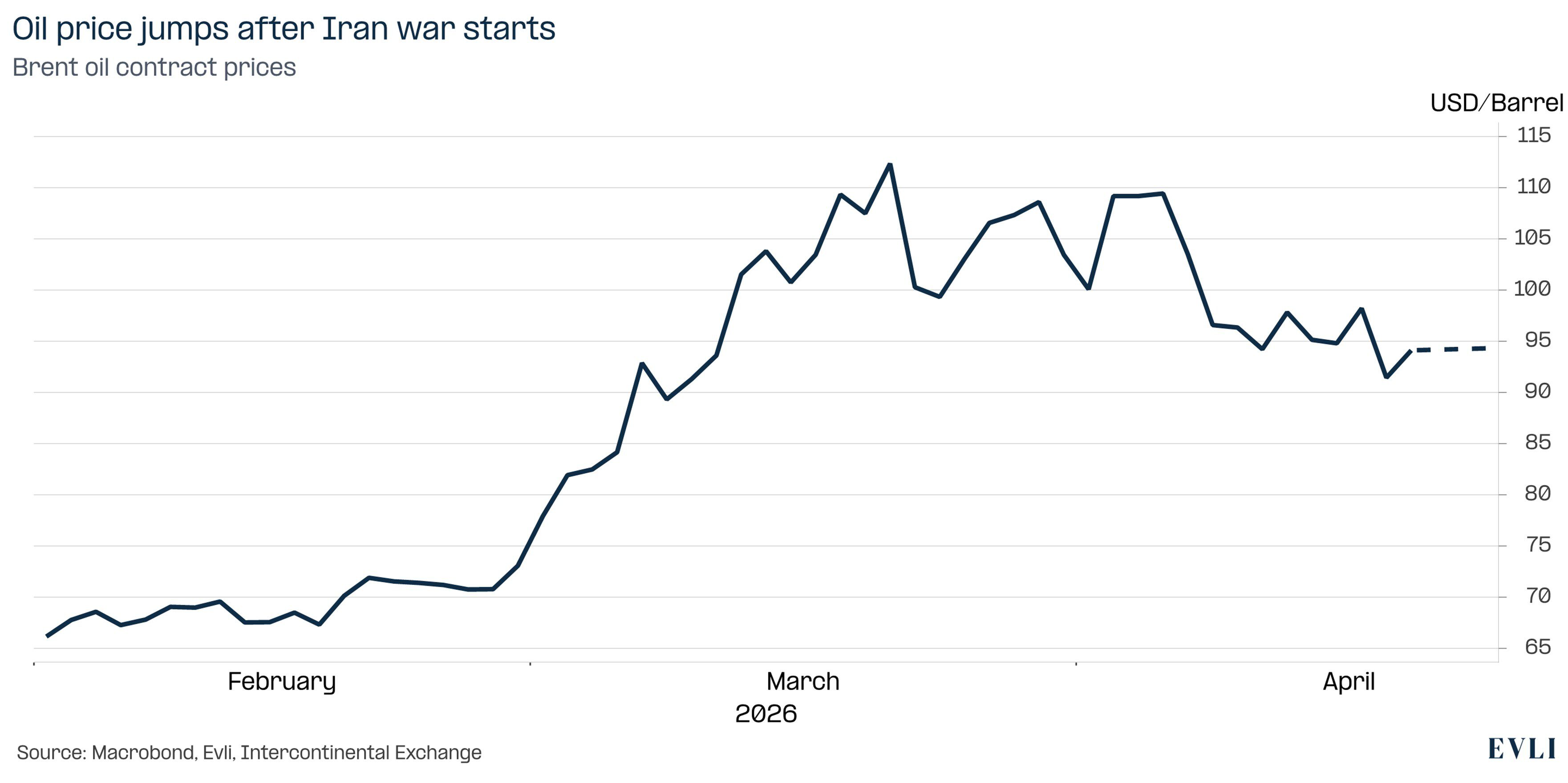

Figure 1: Oil prices have risen significantly as a result of the Iran war

Figure 2: Trump’s approval ratings have continued to fall as a result of the Iran war

Everybody wants to rule the world

Judging by its choices, such as opting for a ceasefire and briefly allowing transit through the Strait of Hormuz, Iran also wants an end to the conflict. Fundamentally, the Iranian regime—like any regime—wants above all to remain in power, and war and the possibility of further military escalation are threats to that power. As much as Iran is depicted as a theocratic power, economics matter. The hardline Islamic Revolutionary Guard, government, and the economy are dependent on oil revenue. The Iranian protests also signal that there is deep dissatisfaction among the populace, and further economic hardship may foster additional disenchantment after decades of dismal economic performance.

Iran's most important ally and largest customer, China, also wants an end to the conflict. China’s domestic demand is weak, housing markets are in a slump, and hence the country's growth rests on investment and exports. A prolonged Iran conflict is a risk to the global economy and therefore to China's export machine.

Iran had to close the Strait to restore its credibility

Iran had to restore its credibility after being humiliated in last year's 12-day war between Israel and Iran. That war demonstrated that Iran could neither inflict meaningful damage on Israel nor defend itself from Israeli bombing. Despite its threats, Iran did not close the Strait of Hormuz. Iranian weakness proved costly. Military action became a more attractive option for the US once Iran was judged to be defenceless and unwilling to close the Strait. Iran had no choice but to close the Strait if it wished to restore credibility.

Pipedreams no longer

Closing the Strait of Hormuz is the deterrent through which Iran ensures that force will not be used against it in the future. The problem with closing the Strait is that the Gulf oil states may attempt to circumvent the Strait by building pipelines and port infrastructure. Saudi Arabia is investing in the East–West Pipeline and in the port infrastructure at Yanbu on the Red Sea. The solution is not ideal, as it still leaves ships susceptible to Houthi strikes.

The United Arab Emirates could expand the Habshan–Fujairah pipeline, which bypasses the Strait. Even Iraq has revived plans for a pipeline linking Basra to the Red Sea port of Aqaba. It is not out of the question that Kuwait could build a connecting line to either the Iraqi or Saudi option. These investments will take years, but if realised, they would dramatically alter the importance of the Strait of Hormuz.

The situation is reminiscent of the Arab oil embargoes of the 1970s, which prompted Western economies to reduce their oil use and develop alternative energy sources. As a result, OPEC's share of global crude oil production fell from roughly 50 percent in 1973 to around 37 percent by 2023. The oil intensity of the global economy, as measured by the barrels of oil used per unit of GDP, has roughly halved over the same period.

By closing the Strait of Hormuz, Tehran has restored its credibility and its deterrent. But the closure may lead the Gulf states to invest in infrastructure that allows them to bypass the Strait. A diminished Strait, in turn, leaves Iran without a credible deterrent. The only remaining path to restoring deterrence would be the development of nuclear weapons—ironically, the very outcome that Israel and the US have sought to prevent through both negotiation and bombing.