The conflict between Iran and the United States appears to have shifted cautiously in a more constructive direction, although the risks remain significant.

The war has lasted for a couple of months, and U.S. President Donald Trump has repeatedly expressed his desire to withdraw from the conflict. Iran has kept the Strait of Hormuz closed to strengthen its negotiating position, but President Masoud Pezeshkian’s statement referring to “sufficient political will” to end the conflict has been interpreted as a signal that Iran considers it has achieved its key objectives.

The markets reacted quickly, but uncertainty remains

A two‑week ceasefire and the reopening of the Strait of Hormuz triggered a clear market reaction: oil prices fell sharply and equity markets rose globally. While the war has weighed on equities and driven interest rates higher, its overall impact on equity markets has remained relatively contained. Nevertheless, both crude oil and interest rate markets continue to price in a meaningful risk of the conflict persisting. At the end of April, crude oil futures turned higher once again.

Negotiations between Iran and the United States remain difficult, hindered by deep mutual distrust, potential internal political fragmentation in Iran, and complex issues related to nuclear disarmament. Our base case is that the overall duration of the conflict and the associated economic damage will remain limited, although the risk of a prolonged escalation remains material

A monetary policy dilemma

The conflict is affecting inflation expectations and complicating the monetary policy outlook. Consumer uncertainty has increased, and global economic uncertainty is weighing on industrial confidence indicators. The German government halved its growth forecast for this year to 0.5% and cut next year’s forecast from 1.3% to 0.9%. The threat of stagflation presents a particularly challenging scenario for the European Central Bank.

Euro area inflation accelerated to 2.5% in March and further to 3.0% in April, driven by an almost 11% increase in energy prices. Economic growth slowed, rising by just 0.1% quarter on quarter and 0.8% compared with a year earlier. At its meeting at the end of April, however, the ECB judged that long‑term inflation expectations had remained anchored and therefore decided to leave its policy rates unchanged.

The U.S. Federal Reserve also kept its interest rate unchanged. Progress was made on Federal Reserve Board appointments after charges against current Chair Jerome Powell were dismissed, allowing Kevin Warsh’s nomination to advance in the Senate. Warsh has previously been regarded as hawkish, but he is expected to advocate a narrowing and reform of the Federal Reserve’s mandate. Powell nevertheless announced that he intends to remain on the Board as a regular member.

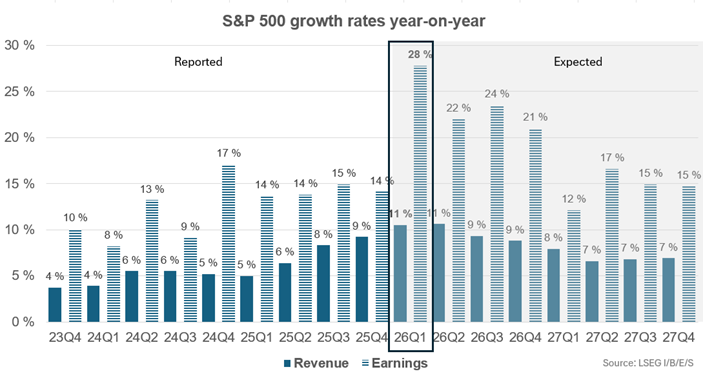

U.S. corporates continue to deliver strength

The first‑quarter earnings season continues to support equity markets, particularly in the United States and other developed markets. Technology companies remain the primary drivers of earnings growth, supported by an investment and demand cycle linked to artificial intelligence. Capital expenditure by the largest cloud service providers is expected to approach USD 800 billion. These figures are historically high and, if realised, would provide a substantial boost to GDP growth.

The results of Amazon, Google and Microsoft significantly exceeded analysts’ revenue and earnings expectations. By the end of the month, around two‑thirds of S&P 500 companies had reported, with eight out of ten beating both revenue and earnings forecasts by clear margins. This positive momentum pushed the index to a new all‑time high of 7,230 points. The market capitalisation of U.S. equities relative to GDP (the so‑called Buffett Indicator) now stands at 2.3x, also at a new record level.

According to media reports, an unlisted company OpenAI may not be on track to meet its growth and profitability targets. The company is being closely watched, as it is expected to be listed later this year. A significant listing from SpaceX is also anticipated in the near term. The expected valuations of both SpaceX and OpenAI are projected to exceed USD 1 trillion, which would place them among the ten largest companies globally by market capitalisation.

Figure: Strong earnings growth among U.S. companies in early 2026