The most valuable IPO in history

The US aerospace and AI company SpaceX is going public with a target valuation of $1,750–2,000 billion. This would make it the world's eighth most valuable public company and the largest IPO in history. Elon Musk would be the majority owner of two public companies valued at over a trillion dollars, as he also leads the electric vehicle company Tesla.

The IPO market is running hot; two other AI companies, Anthropic and OpenAI, plan to list later this year. These companies are also targeting market valuations exceeding one trillion dollars.

SpaceX disrupted the aerospace industry

Legend has it that in 2001, Musk traveled to Moscow to buy a refurbished Russian ballistic missile to launch greenhouse experiments to Mars. Russian aerospace executives did not take him seriously, and allegedly one even spat on his shoes. On his flight home, Musk decided to build his own rockets. SpaceX was founded the following year.

Before SpaceX, the rocket industry was a Cold War relic. United Launch Alliance (ULA), a joint venture between Lockheed Martin and Boeing, dominated the space launch market, with the US Air Force as its largest customer. There was little competition. Hence, the incumbent ULA had no incentive to develop new technology nor to reduce costs. In turn, the primary source of demand, the US Air Force, had little incentive to lower costs as it was a public entity.

Between 2013 and 2016, a single ULA launch cost $350–450 million. The market disruptor SpaceX offered launches for $60 million, yet the US Air Force still chose ULA. SpaceX sued the Air Force, forcing the market open to competition. Cheaper prices and successful rocket launches eventually earned SpaceX the trust of US agencies. According to SpaceX’s pre-IPO S-1 filing, the company launched over 80 percent of the world’s total annual payload mass into orbit in 2025.

SpaceX disrupted the oligopolistic aerospace industry by developing reusable rocket engines, which significantly lowered launch costs. Contemporaries viewed Musk's proposal for reusable rockets as near impossible. These rockets have been central to establishing Musk's reputation as a technological pioneer.

The Musk universe: Disruptive and vertically integrated

Musk and his companies are fundamentally disruptive. Tesla disrupted the automotive industry by electrifying it. Advances in battery technology made electric vehicles possible, just as Nvidia's GPU accelerators now enable AI. The legacy automakers dominating the industry—Toyota, Volkswagen, Ford, and GM—remained reliant on the internal combustion engine, lacking the incentives to drive meaningful innovation.

Another parallel between SpaceX and Tesla is their control over the supply chain, from components to the finished product, rather than relying on subcontractors. Musk’s companies are highly vertically integrated, handling multiple production steps internally to capture cost and efficiency benefits.

Traditional players in the automotive and aerospace industries are far less vertically integrated. Automakers purchase engines, electronics, and seats from suppliers, assemble them, and sell them through dealerships. Rocket manufacturers previously ordered engines from Russia, structural components from dozens of defense subcontractors, and utilized state-owned launchpads.

Tesla designs and manufactures part of its battery packs, electric motors, software, and Autopilot system in-house. It sells cars directly to consumers, bypassing traditional dealership networks entirely.

SpaceX designs and manufactures its own rocket engines, structures, avionics, and guidance systems at its factory in Hawthorne, California. It also owns and operates its own launchpads in Boca Chica and Cape Canaveral.

However, vertical integration does not stop at the rocket: SpaceX designs and manufactures its Starlink satellites, launches them on its own rockets, operates the satellite network, and sells internet connectivity directly to end users. SpaceX takes vertical integration to the extreme.

In Tesla's case, Chinese EV manufacturers have learned from and applied Tesla's methods. The company’s Shanghai Gigafactory created an ecosystem in China that led to Chinese EV companies becoming "Tesla killers." The same forces that drove Tesla's success now threaten its very existence.

Tesla's decision to pivot toward becoming a robotics manufacturer may partly be a desire to escape from the EV price wars—though the challenge remains that Chinese companies operate in robotics as well. SpaceX does not face the same relentless Chinese competitive pressure. If the company stayed within its core matrix as an unmatched combination of rockets and satellites, and if its valuation were reasonable, SpaceX could be an excellent investment.

Space and Starlink satellites form SpaceX’s profitable core

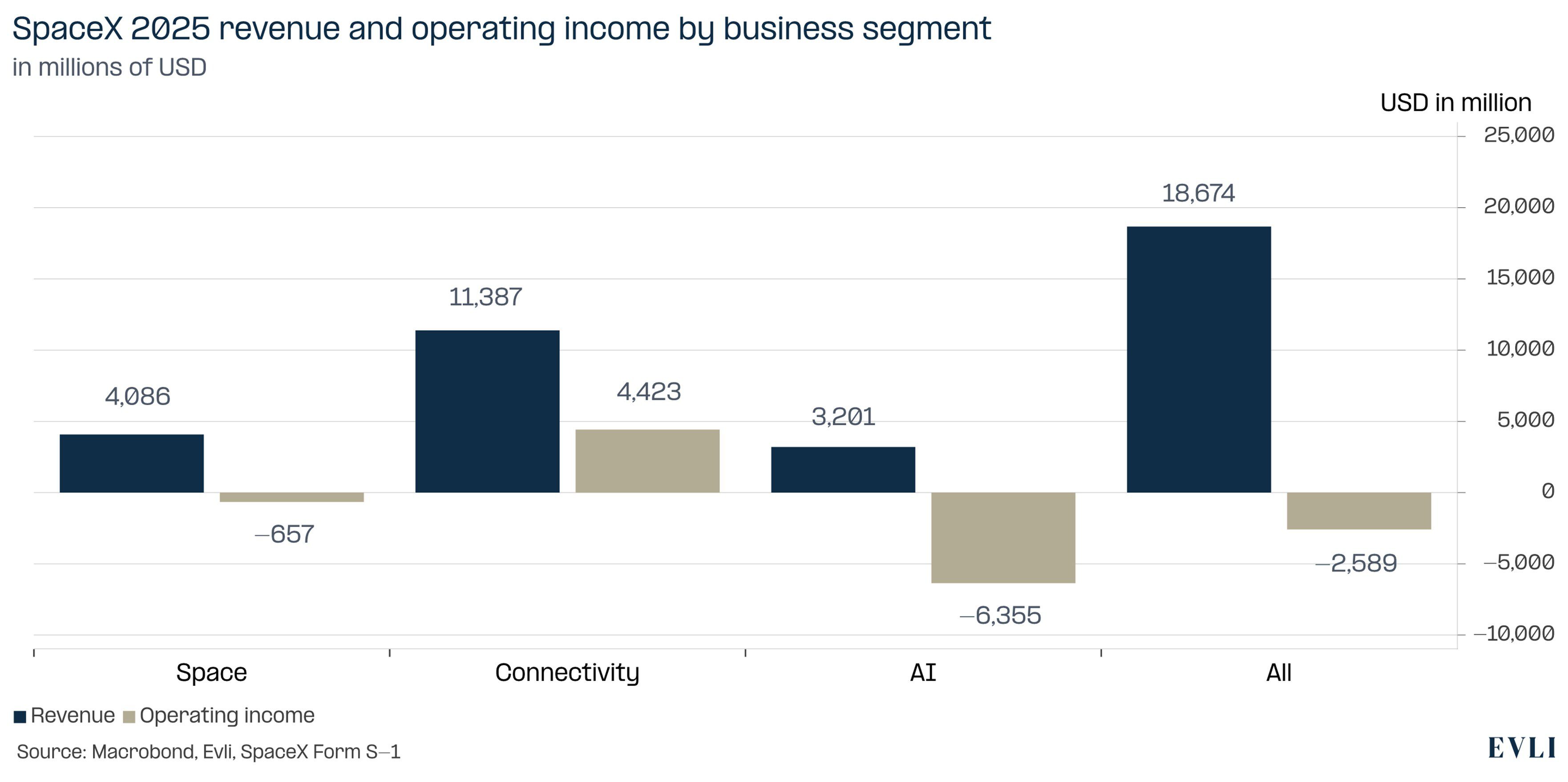

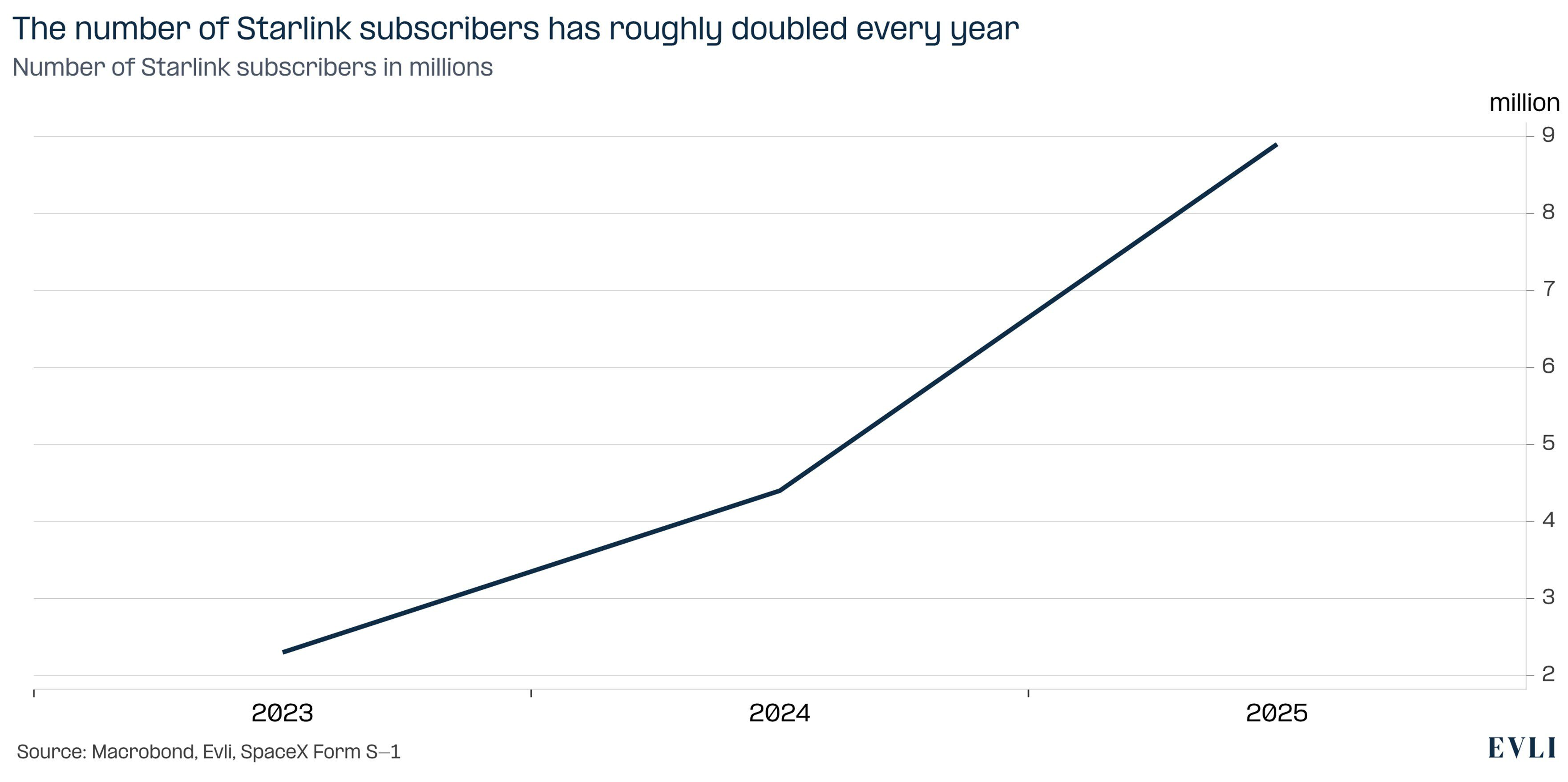

In 2025, the satellite unit Starlink generated $11 billion in revenue, accounting for roughly 60 percent of SpaceX's total revenue. Starlink's subscriber base grew from 2.3 million at the end of 2023 to 10 million by the end of February 2026. Its revenue grew by roughly 50 percent last year. Starlink is highly profitable, generating $4.4 billion in operating profit, a 120 percent increase compared to 2024. The operating margin rose from 26 percent to 39 percent, an exceptionally high margin for a capital-intensive industry.

Starlink currently enjoys a functional monopoly. The industry will likely evolve into a duopoly once Amazon deploys its competing Low Earth Orbit (Leo) satellite service. Amazon's Project Leo (formerly known as Kuiper) is years behind, and duopolies are often highly lucrative for both parties—similar to how Google, Meta, and Alphabet dominate the high-margin advertising space.

SpaceX's aerospace unit consists of launch operations. It dominates the global launch market with an over 80 percent market share and launches the company’s own satellites. The unit’s revenue grew 8 percent from $3.8 billion to $4.1 billion. The unit would be profitable, but developing the next-generation Starship rocket consumed $3 billion in 2025.

The synergistic combination of rockets and satellites provides an excellent competitive advantage. Growth is rapid and barriers to entry are high, keeping margins elevated.

The AI unit – An achilles' heel?

In February, SpaceX changed completely. The company acquired another Musk venture, the AI company xAI. In 2025, xAI generated $3.2 billion in revenue but incurred an operating loss of $6.4 billion. The AI unit pushes the consolidated SpaceX entity deep into the red.

SpaceX's AI model, Grok, has performed reasonably well in LLM benchmarks. The problem lies in distribution: the AI has been sold through the X platform (formerly Twitter), but engagement collapsed after the initial hype. Due to insufficient demand, the utilization rate of the Colossus 1 data center cluster hosting the model is only 11 percent. Expensive chips have been left sitting idle.

Musk’s solution has been to lease the Colossus 1 data center cluster to rival AI company Anthropic. Anthropic pays SpaceX $15 billion annually to lease the 300-megawatt data center, underscoring the massive value of AI infrastructure. Notably, the Colossus data center contains older 2022-generation Hopper accelerators, yet still generates $15 billion a year. This is roughly equal to SpaceX’s entire 2025 space and satellite revenue.

Leasing the underutilized data center to a competitor allows for a back of the envelope opportunity cost calculation. SpaceX also owns the larger, 700-megawatt Colossus 2 data center cluster, equipped with more next-generation Nvidia Blackwell accelerators. Simple math suggests this center could command roughly $35 billion a year in rent if leased out.

By leasing its data centers, SpaceX's revenue would jump from $18.7 billion to $65.5 billion, and operating margins could match asset-light tech giants like Visa.

Instead, Musk believes the future value is so high that he prefers to absorb the losses, betting heavily on training next-generation AI models and developing next-gen space rockets. Data center infrastructure companies like Nebius and Coreweave also do not command the same high valuation multiples in public markets as aerospace companies.

The Amazing Race

The AI race demands massive capital outlays, pitting SpaceX against the world's largest tech giants: Alphabet, Microsoft, Meta, and potentially the upcoming IPOs Anthropic and OpenAI. Highlighting the stakes, Google co-founder Larry Page has stated he would rather go bankrupt than lose the AI race.

Even if SpaceX succeeds in developing top-tier models, it lacks a strong distribution channel. Google has Android and Chrome, Microsoft has Office, and Meta has social media. OpenAI may soon reach one billion users, and Anthropic has achieved cult status among developers. The best technology does not always win, and it is not even clear that SpaceX will develop the best models.

It is strange that the AI race is framed as winner take all. Monopolies are rare outside of natural monopolies like electricity distribution. An oligopoly is the more common market configuration in private markets.

Oligopolies will likely emerge in AI as well. Anthropic, Google, OpenAI, and Microsoft could carve up the enterprise market, while Google and OpenAI split the consumer side. Models may also specialize; for instance, Meta’s models have tailored applications toward healthcare. In this context, the relative edge and role for SpaceX’s AI remains unclear.

Musk has also pitched the company as an AI infrastructure player by discussing space-based data centers. Economically, space-based data centers are not viable today, and it remains entirely unclear on what timeline or terms they would become profitable.

Astronomical valuation

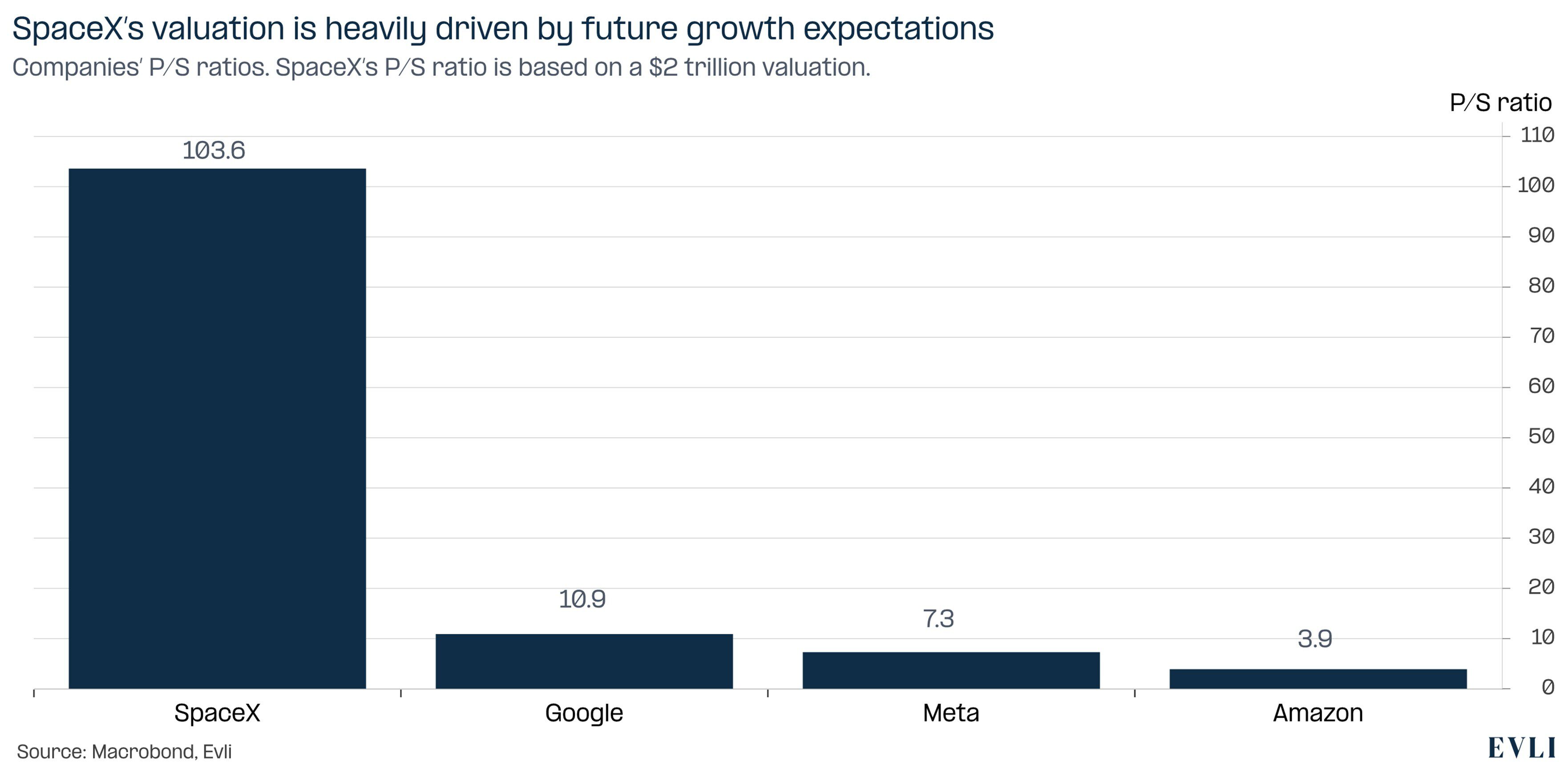

As an investment, the company is problematic due to its astronomical valuation. SpaceX's 2025 revenue was $18.7 billion, yet it targets a market capitalization of $1,750–2,000 billion. The company’s Price-to-Sales (P/S) multiple would be around 100.

With such a lofty market cap SpaceX would eclipse Meta Platforms, which has a market cap of roughly $1,500 billion. SpaceX's 2025 revenue was $18.7 billion against Meta's $201 billion. SpaceX posted an operating loss of $2.6 billion, while Meta generated $83.3 billion in operating profit—roughly five times SpaceX’s total revenue. In terms of valuation, SpaceX is also reaching for the stars.

Figure 1: SpaceX business segment revenue and operating profit for 2025

Figure 2: SpaceX's valuation is exceptionally high, no matter the benchmark

Figure 3: The Starlink user base has doubled annually

SpaceX is Musk’s vision incarnate

Elon Musk owns roughly 42 percent of SpaceX shares and controls 85 percent of the voting power. This concentration of voting power is extraordinary, but the ownership structure reveals what a SpaceX investment ultimately is: a bet on Musk’s vision and leadership.

SpaceX's valuation can only be predicated on a very lucrative future. The company is risking everything on the future—next-generation rockets and AI models. Tesla's market history shows that the fundamentals of Musk's companies and their stock prices often move independently. Instead, the share price acts as a barometer of faith in Musk's vision. This will hold true for SpaceX.

SpaceX is Musk’s vision incarnate. That may encompass: a Mars colony, data centers in space, and perhaps a merger with Tesla. What is certain is that Musk's visions will shift, ebb and flow along the way. Much like good science fiction. Investing in SpaceX means investing in Musk. For better or worse.