A dystopian vision of a world, where AI has demolished the moats of technology companies and driven the economy into mass unemployment, has captured the market's imagination. While AI is transforming industries and many companies will not survive the transition, several tech firms remain immune to AI for the foreseeable future, and many stand to benefit from it. Mass unemployment or the "end of work" is as implausible now as it was with the advent of the steam engine, railroads, telephone, internet, or other technological disruption.

A brief history of AI fears

The stock market has been on a strong upward trajectory since the October 2022 lows, fuelled by robust economic and earnings growth. Alongside this growth, AI has been a cornerstone of the bull market. Global stock markets have become increasingly skewed towards technology, with roughly half of the S&P 500 index and a third of global stock markets being composed of technology companies. Hence, AI-related news has also become a primary source of market turbulence.

AI fears have evolved alongside the technology. Initially, the concern was a repeat of the 2000s dot-com bubble. This currently seems far-fetched, as the Nasdaq’s P/E ratio sits slightly above 30, compared to a staggering 200 at the peak of the IT bubble. Despite this, Bank of America’s fund manager surveys still list a "dot-com crash" as the most cited tail risk. The irony of surveying tail risk is of course that a tail risk is a risk no one sees coming.

As AI investments climbed into the hundreds of billions, a new worry emerged: what if AI returns end up being much lower than envisioned? This fear is two-fold: what if AI is underwhelming in terms of productivity gains, and what if it cannot be monetised due to, for instance, cheap Chinese AI models? The underwhelming narrative was supported by anecdotal evidence, such as an MIT survey where most users found AI nearly useless, and by Microsoft’s Copilot solutions, which many consider a distinct disappointment.

On the commercialization front, the problem is that AI models are expensive to train but cheap to imitate. These concerns escalated a year ago when China's DeepSeek released a model nearly on par with American flagship models at a fraction of the cost. By training on the outputs of top-tier models and optimizing for cost-efficiency, the Chinese are able to emulate top AI models while American companies foot the bill for expensive training runs. This pattern repeated again this year, though with less media fanfare.

From Utopia to Dystopia

The latest fear is the antithesis of the old one: instead of dreading that AI won't meet lofty expectations, the market now fears that AI will overpower software and other knowledge-based sectors. Or at least, AI will lead to radical margin compression, in effect shifting market structure from oligopolistic closer to perfect competition.

This new strand of AI anxiety has both micro and macro dimensions. A prime example is a February 23 Substack piece by Citrini Research’s James van Geel, which triggered significant selloffs in cited companies such as Visa, Mastercard, Blackstone, Apollo, and DoorDash.

In Citrini’s macro-dystopia, AI devours white-collar jobs. Historically, technology displaced workers: workers moved from agriculture to manufacturing, and then, with new shocks, from manufacturing into services. This time, however, it targets high-income roles like software engineering. In this grim view, IT professionals end up driving Uber—until robotaxis take those jobs as well.

Yet, history suggests a different path. Despite centuries of productivity growth, the total amount of work has not decreased. People simply move to new roles or take on new tasks. Many of today’s professions didn’t even exist before WWII. It must have been difficult to imagine some of the present occupations in the 1930s. It is similarly difficult now, but that does not mean it won’t happen. The market will find ways to deploy labour based on demand, just as it has been before. This will, of course, mean catastrophe for some who have invested in a now obsolete skillset for decades. But in aggregate, productivity will rise and the economy will adapt.

The Tower of Babel

In the biblical story of Babel, humans all spoke one language. Language allowed co-ordination, and in their hubris, humans sought to build a tower into the heavens. Angered, God confused human language into many languages so that humans could no longer build their tower.

Software companies literally moved services to the cloud, which allowed for the most lucrative business model in the world. Software as a service (SaaS) companies regularly have 80 percent gross margins, whereas retail and manufacturing have 20 –30 percent gross margins.

Software companies have been the darlings of markets and private equity for years, offering double-digit revenue growth, the best margins in the market, and asset-light balance sheets.

Software companies allow people to interact with computers by effectively translating human language into machine language. But with new AI models, such as Anthropic’s Claude Cowork and OpenAI’s Codex-Spark, a user can bypass software and instruct a computer in natural language. Tasks could include tax planning or filing travel expenses. The market's question is simple: why pay for expensive software if there is no need for a translator?

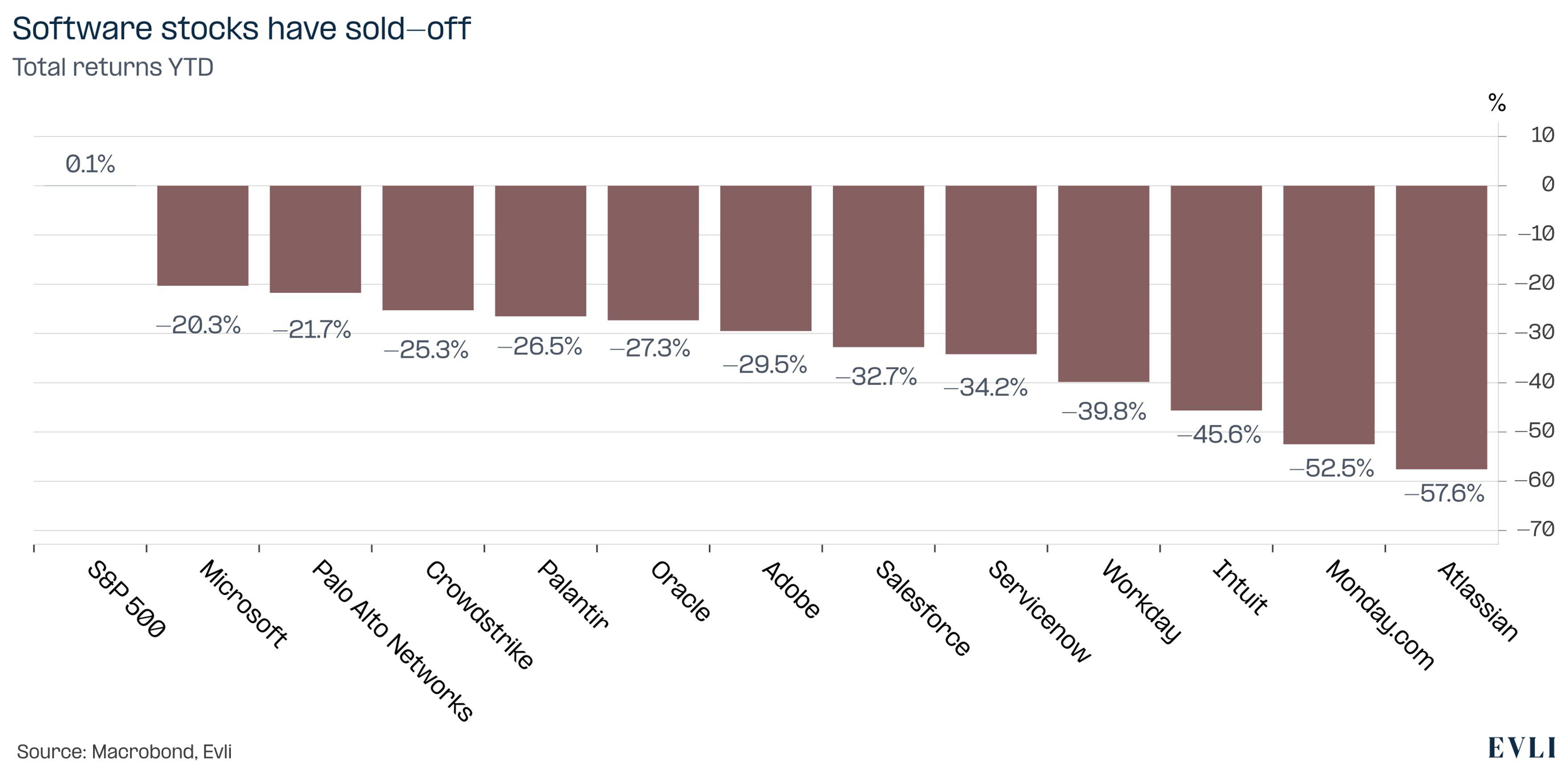

Crucially, disruption isn't yet showing up in the numbers. In the latest earnings season, firms like Microsoft, ServiceNow, HubSpot, Datadog, and monday.com saw revenues grow by roughly 20 percent year-on-year. But the market is forward-looking. Investors pay high valuation multiples for predictability and growth, both of which are now under scrutiny.

AI threatens the software business model by lowering switching costs. Most software is billed per-user. If AI makes programming more efficient, companies may need fewer programmers and, consequently, fewer licenses. Furthermore, the cornerstone of software market power is high switching costs. If switching is easier, competition will increase and hence margins will decline.

Figure 1: Software companies’ share prices have fallen sharply since the beginning of the year

Dating Apps and Nuclear plant software

The magnitude of the AI threat varies by company. In retrospect, the panic may seem overstated in many instances. Constellation Software has seen its stock nearly halve. The company owns a vast array of small, vertical software firms like AgriSoft, which provides chicken coop software. The niche software tracks operations from egg hatching to feed consumption. These systems are mission-critical; a single error is existential for the farm. A farmer is unlikely to risk their entire operation by switching to an unproven AI solution for a modest reduction in costs that are a small portion of overall costs in the first place.

AI is a statistical rather than a deterministic model. Models hence give answers that are likely correct. Models may hallucinate, and hence the exact same answer may be impossible to replicate. While hallucinations are decreasing, even a theoretical probability of error may be too much for critical systems like nuclear power plants or core banking systems. Moreover, companies that own proprietary, high-value databases—like Moody’s or S&P Global—are more likely to be AI winners than victims. As time goes on companies will ringfence their valuable databases and leverage their own data to a greater extent.

The market seems to assume AI winners must be outsiders. While bookstores and video rentals failed to adapt to the internet, today’s targets are technology companies themselves, which are inherently better positioned to pivot. Less than a year ago, Google was written off as an AI loser; today, its Gemini model is a top-tier competitor, its search ad revenue continues to grow at close to 10 percent, and the stock has more than doubled from its lows.

As Spotify's Co-CEO noted, technology is only truly disruptive when it forces a change in the business model. For Spotify or Netflix, the model remains a mix of ads and subscriptions; AI doesn't change that logic —it simply makes recommendations and ad targeting more efficient.

Conclusion

AI will certainly change the digital landscape, but the market has prematurely decided that the majority of tech companies will be victims. While some will struggle and valuations may not return to former heights, many software firms are virtually immune to the AI threat, and many will emerge as beneficiaries.