The market environment in June was split. On the one hand, strong equity market performance, declining oil prices, and a partial easing of tensions in the Middle East have supported risk appetite. On the other hand, persistent inflation, increasingly hawkish central bank communication, and the narrow, technology-driven nature of the market rally have added to uncertainty.

The preliminary agreement between the United States and Iran has reduced immediate geopolitical risks, but a final peace agreement remains unresolved. Traffic through the Strait of Hormuz is gradually normalising, although the after-effects of earlier supply disruptions in energy markets may keep oil prices elevated and inflationary pressures higher than expected for longer.

ECB hawks remain vigilant

The inflation outlook has become more challenging, particularly in Europe, where global supply shocks have a stronger impact on the economy than in the United States. Euro area growth forecasts have been revised downwards, while inflation has remained above the ECB’s two percent target.

The decline in crude oil prices back to pre-crisis levels in the Persian Gulf is rapidly easing upward pressure on consumer prices. However, core inflation and producer price dynamics still point to ongoing cost pressures. As expected, the ECB raised its key interest rate to 2.25 percent in June. Market expectations for further rate hikes eased somewhat following the drop in oil prices.

US economic outlook remains positive

In the United States, economic growth and labour markets have remained robust, giving the Fed room to prioritise price stability over growth concerns. The Fed’s communication has turned more hawkish, reinforcing market expectations of another interest rate hike later this year.

Job creation has exceeded both early-year figures and economists’ expectations for three consecutive months. Private consumption and investment are expected to sustain economic growth above two percent this year. Growth in the second quarter is estimated to have reached as high as three percent.

Growing caution in equity markets

The sharp equity rally moderated in June, although most markets still posted gains of a few percent. Market sentiment has become more cautious. In the United States and Asia, the share of technology companies in total market capitalisation has risen to exceptionally high levels, and sentiment indicators suggest signs of overheating.

Artificial intelligence remains the key driver of equity returns, but also represents the most significant market risk. Strong growth in AI-related investments, along with robust demand for data centres, memory, and other components, has doubled semiconductor stock prices in just three months. This rally has also been supported by substantial earnings improvements.

SpaceX initiated the expected wave of mega-IPOs by offering shares to the market worth USD 75 billion - less than five percent of its total share capital. At current prices, SpaceX’s market capitalisation stands at USD 2.1 trillion, making it the sixth-largest company globally. Comparable mega-IPO activity is expected from AI companies Anthropic and OpenAI later this year.

From an investment perspective, an overweight in equities has been justified by strong earnings growth, the ongoing investment cycle, and the AI theme. However, the risk of a short-term correction has increased. The medium-term outlook for equities remains reasonably positive. Key variables include inflation trends, central bank communication, the direction of oil prices, rising long-term interest rates, and the earnings outlook for the technology and semiconductor sectors.

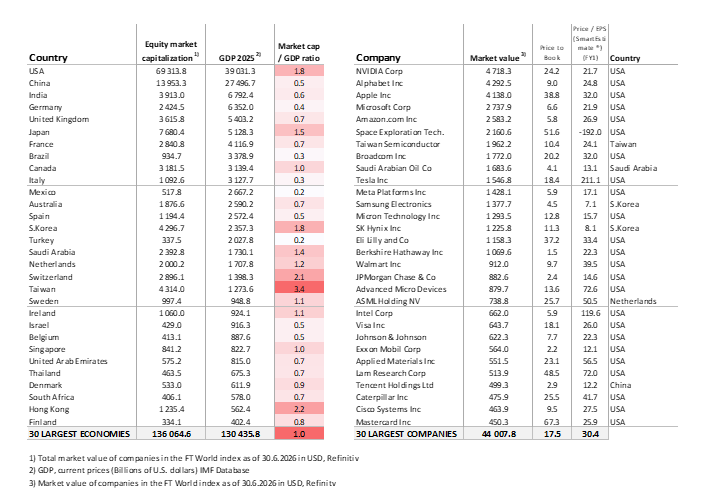

Table: Largest economies and companies globally