Technology ascendant

Broad technology's share of global equity market capitalization has grown to historical highs and now exceeds the peaks of the dot-com bubble at the turn of the millennium. The rise of technology stocks is an international phenomenon. In the United States, technology stocks account for roughly 40 percent of the market, in emerging markets about half, and in Japan roughly a fifth. Europe is the exception that proves the rule, as the share there is below ten percent. Exact definitions are tricky as technology indices may not include companies such as Alphabet or Amazon.

The technology industry is the poster child of globalization with supply chains spanning the US, Japan and East Asia. Software and chips are designed in the United States, but the chips are manufactured in China, Korea and Taiwan. Japanese companies supply the machinery and equipment to the semiconductor fabs. Stock markets reflect this division of labour with the US composed of software and hyperscalers, Japan of semiconductor equipment companies, and Taiwan and Korea consisting of semiconductor fabrication companies. China is developing most of technology stack although large parts such as Huawei are unlikely to be listed.

Investing has traditionally meant tracking and anticipating macroeconomic indicators. This approach is justified when global markets consist of thousands of companies drawn from different sectors, so one can assume some crude approximation of the law of large numbers. Because of the technology sector's dominance, however, one cannot just ignore technology as an independent factor. The key to the performance of and within the technology sector is of course AI.

AI is a general-purpose technology or GPT, meaning it improves productivity broadly rather than in just one specific area. Earlier general-purpose technologies included steam, electricity and the internet. Earlier AI, though, is perhaps general-purpose technology in its purest form. What could be more general than gaining understanding through better models?

Semiconductor companies are making record profits

The infrastructure enabling AI is being built out rapidly. Naturally in this early phase, profits flow to the infrastructure builders. AI infrastructure is largely data centers, which are shells containing hundreds of thousands of semiconductors. The infrastructure is, hence in fact, advanced semiconductors.

AI models are computed using AI accelerators, which are a combination of logic and memory chips. The logic chip does the calculations whilst communicating with its memory chips. The principle is the same as with a computer.

In 2019, the 15 most valuable listed companies included only a single semiconductor company. Presently there are as many as six. At the top of list are Nvidia and Broadcom, which design AI accelerators. Also included are Taiwan's TSMC, which manufactures logic chips, and the memory makers Samsung, SK Hynix and Micron. Once could make the argument there are even more semiconductor companies on the list as Google and Amazon also design AI accelerators and operate fleets of data centers.

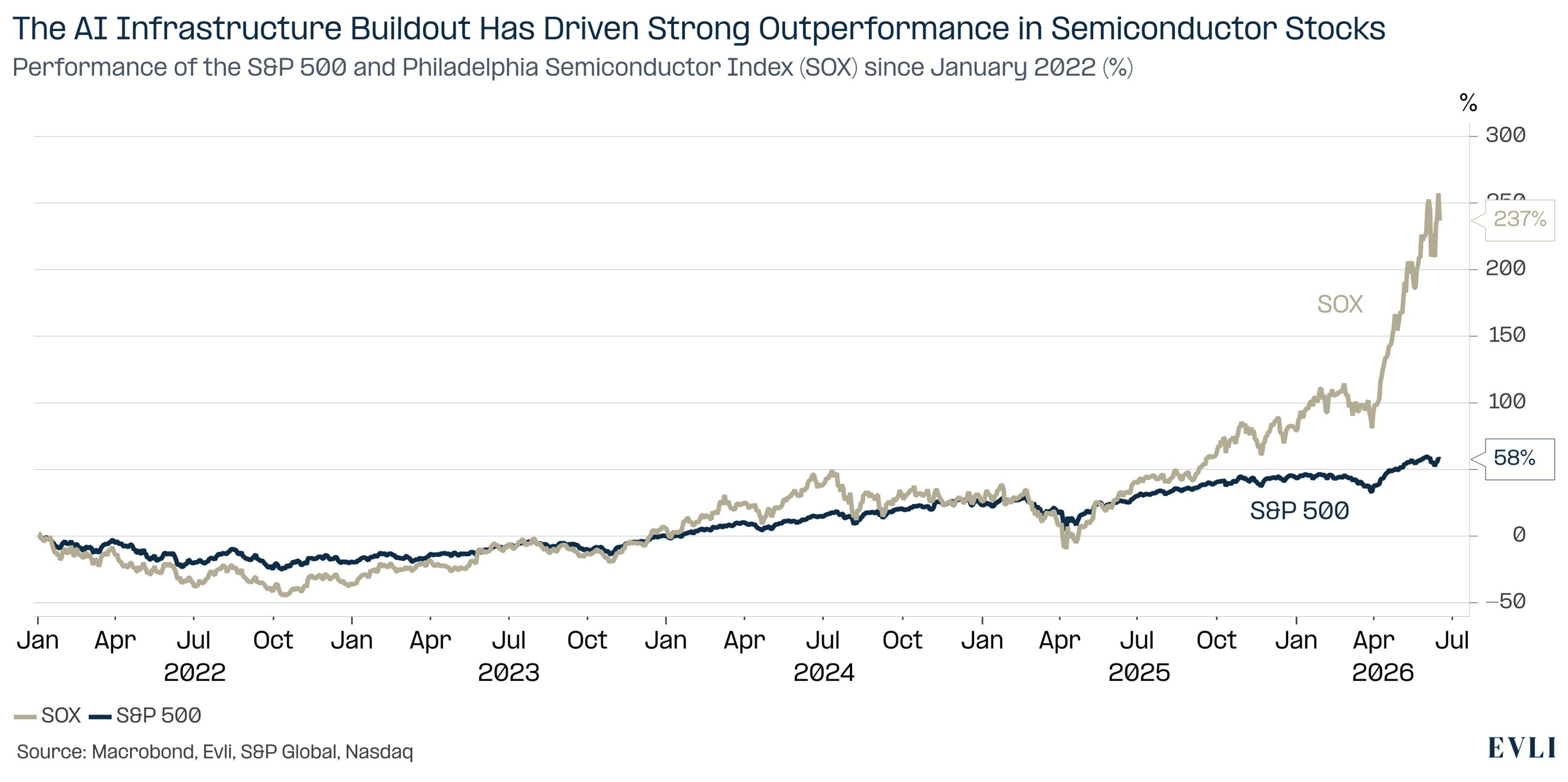

Figure 1: The AI infrastructure buildout has driven strong outperformance in semiconductor stocks

The semiconductor industry is a cyclical business

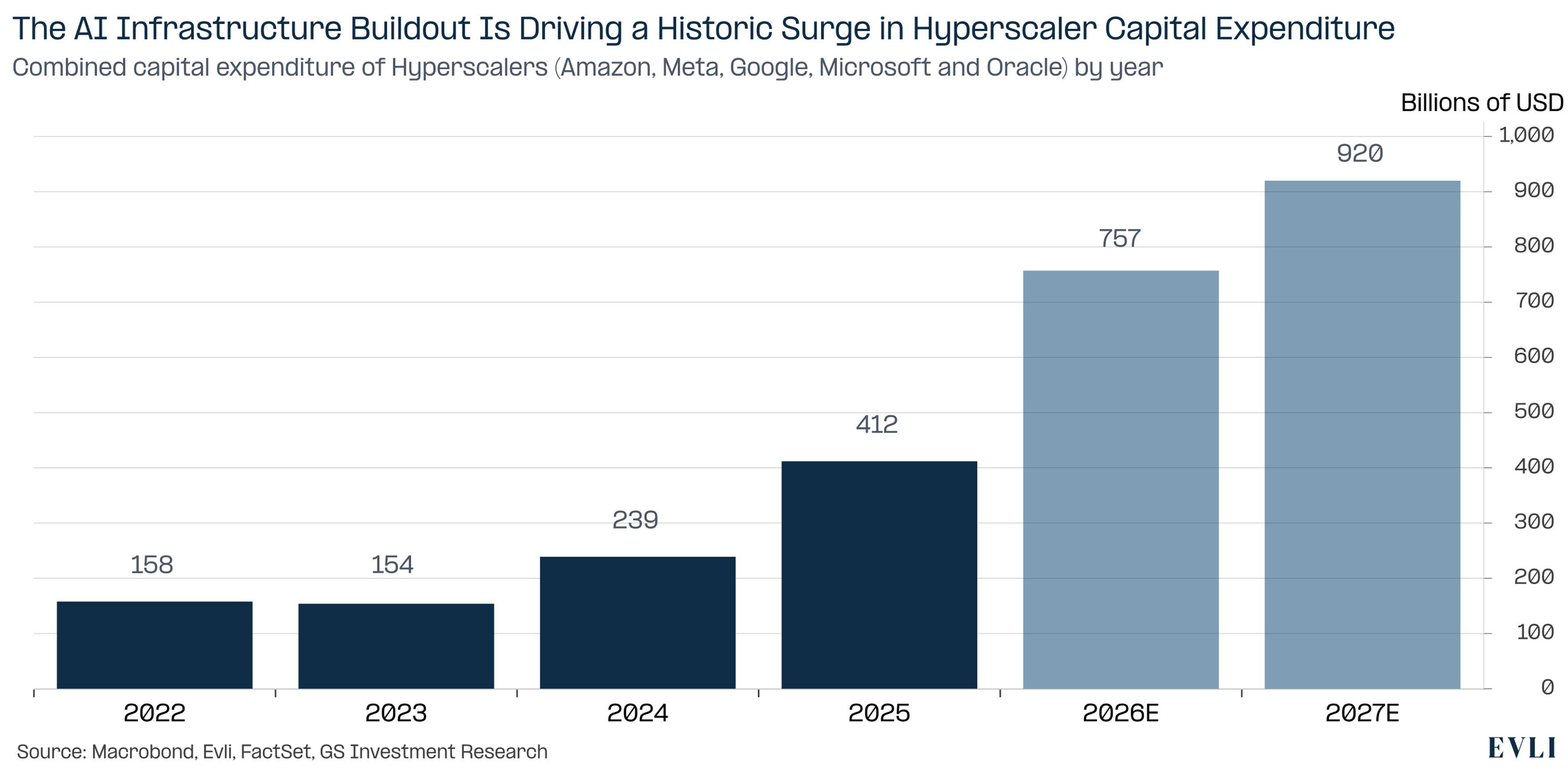

Semiconductor companies' market values have risen rapidly along with surging profits. The companies buying chips are primarily the world's largest technology firms including Amazon, Alphabet, Microsoft and Meta and the AI model companies Anthropic and OpenAI. These firms are spending up to hundreds of billions on chips. Next year the sum will grow further still.

Demand for chips continues to outpace supply, and the chip factories or fabs are running at full capacity. As a result, chip prices have multiplied in places, which is the reason for the semiconductor companies' fabulous profits. The memory maker Micron has said it cannot accept all customer orders, and customers have signed contracts committing to pay high prices for years to secure their memory supply.

Semiconductor players' high profits have driven them to invest in additional capacity. High profits also attract competition, such as Chinese players, which are however hampered by export restrictions on semiconductor manufacturing equipment. New fabs will add supply, and as a result margins will eventually decline. The question is when.

The semiconductor industry is the canonical cyclical industry. The boom bust sequence played out in the semiconductor industry as PCs became widespread in the 1990s, again as smartphones spread in the 2010s, and most recently in the aftermath of the pandemic, when every good was seemingly in short supply. The rise in prices and profits is followed by overinvestment that leads to oversupply and a fall in prices and profits.

The boom bust cycle and ever-increasing cost of next generation fabrication plants has led to industry consolidation. In the 1980s there were dozens of significant players in the field, whereas today there are three large ones including Samsung, SK Hynix and Micron, with the Chinese companies such as CXMT gaining market share.

The present cycle may very well be the most powerful semiconductor boom bust cycle to date. It takes more than two years to build and ramp up a memory fabrication plant, and companies' order books are full, so memory supply will not keep pace with demand in the coming years. Extreme demand does not however alter the underlying boom-bust dynamics of semiconductor economics.

The length and magnitude of the current cycle are directly proportional to the duration and magnitude of the AI cycle, which is set to be substantial. Consensus estimates of large technology company capex for 2027 are climbing towards a trillion dollars.

Technology companies are emboldened because their own data center order books are also surging, which provides visibility. Where as dot.com era orders were driven by orders anticipating future demand, AI orders are about servicing actual demand. Additionally, and perhaps more importantly large technology may companies fear not investing in AI means being left out of markets in the future. Hence investing in AI is also a strategic imperative relating to survival. According to investor Gavin Baker, Google co-founder Larry Page has said internally at the company that he is willing to go bankrupt rather than lose the AI race.

Figure 2: The AI infrastructure buildout is driving a historic surge in hyperscaler capital expenditure

Who extracts value in the AI ecosystem?

The total size of AI returns and the distribution of those returns are the primary questions in investing. Will the profits go to the developers of AI models such as Google, Anthropic, OpenAI and SpaceX? Or to the service providers, such as the software companies Microsoft, Salesforce and Adobe? The tech giants are attempting to improve their economics and hedging their bets through vertical integration. Ultimate integration involves fielding a fleet of data centers, designing custom AI accelerators and AI models, and offering services that leverage AI models. Alphabet has so far been the only large technology company that has been able to span the entire AI stack. Microsoft and Meta are attempting the same.

The key question for the division of profits may be the role of AI models. Will AI models become a standardized product that are effectively interchangeable? In that case the service providers, such as Microsoft and a host of software companies would extract most of the economic value in the AI economy. Or will the models subsume the service layer rendering the service layer mute. The service layer would be much like data center hull, a piece of cement encapsulating a cluster of highly valuable chips. This idea has brought down the stock prices of software companies. The question of who extracts value will become ever more topical when the AI companies Anthropic and OpenAI list on the stock market, possibly later this year.