Co-investments have become a core part of private equity portfolios, making deal quality more important than ever. Our research across more than 8,000 deals examines whether limited partners are getting access to the best opportunities.

Co-investments have moved from niche allocation to core portfolio building block. As more capital flows into direct deal participation alongside general partners (GPs), the strategic question for limited partners (LPs) is no longer whether to co-invest, but whether the deals offered alongside fund commitments represent genuine GP conviction: the best ideas, offered to the most trusted partners.

The question has been studied before, with mixed results. Fang, Ivashina and Lerner (2015), in a widely cited study of 179 co-investments, found that co-investments underperformed fund investments, raising concerns about the quality of deals offered to LPs. Braun, Jenkinson and Schemmerl (2020), working with a larger sample of approximately 10,000 deals, found no systematic underperformance.

Our study builds on this work with greater scale and a methodological improvement: a three-way comparison design. Evli’s proprietary fund-of-funds dataset spans over 8,200 deals and $1,25 trillion in deployed capital. Crucially, it distinguishes between confirmed co-investments, confirmed non-co-investments and the broader deal universe. This three-way design allows us to test whether our results are driven by how the comparison group was selected.

The results show they are not: the broader deal universe performs almost identically to confirmed non-co-investments, validating the comparison framework.

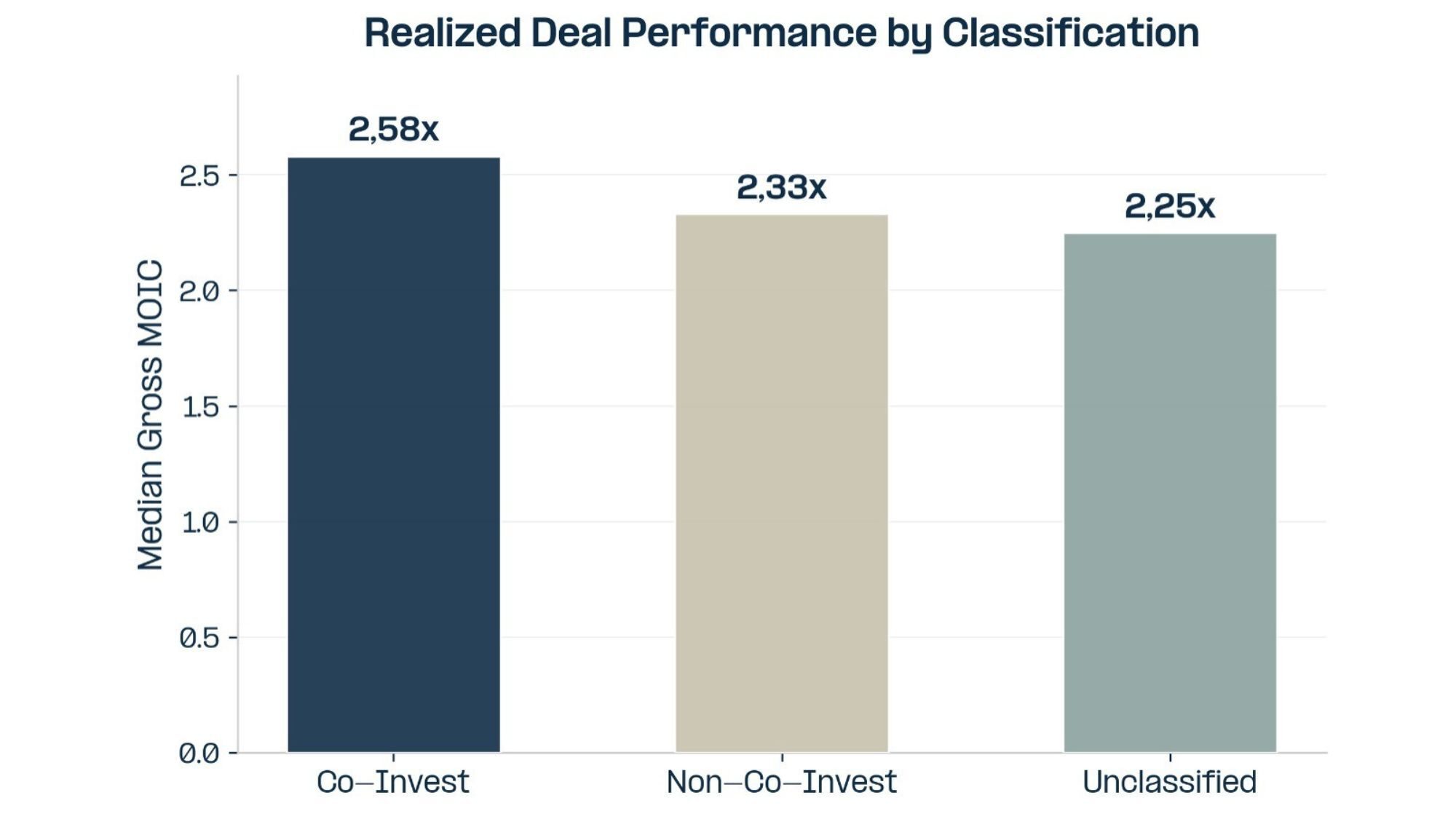

Co-investments returned more and lost less

Among realized deals, co-investments returned more and lost less across every metric.

| Co-Investment | Non-Co-Investment | All Other Deals | |

| Deals analyzed | 613 | 382 | 4,143 |

| Median return (MOIC) | 2.58x | 2.33x | 2.25x |

| Loss rate | 18.1% | 25.7% | 25.3% |

| Severe loss rate | 12.7% | 20.4% | 19.7% |

The findings are consistent for both MOIC (Multiple on Invested Capital) and IRR (Internal Rate of Return). Returns are measured using MOIC, which compares the total value returned to the capital originally invested. All return figures in this article are gross of fees and carried interest, isolating deal quality from fee structure. This is the right lens for evaluating whether GPs offer strong deals to co-investors.

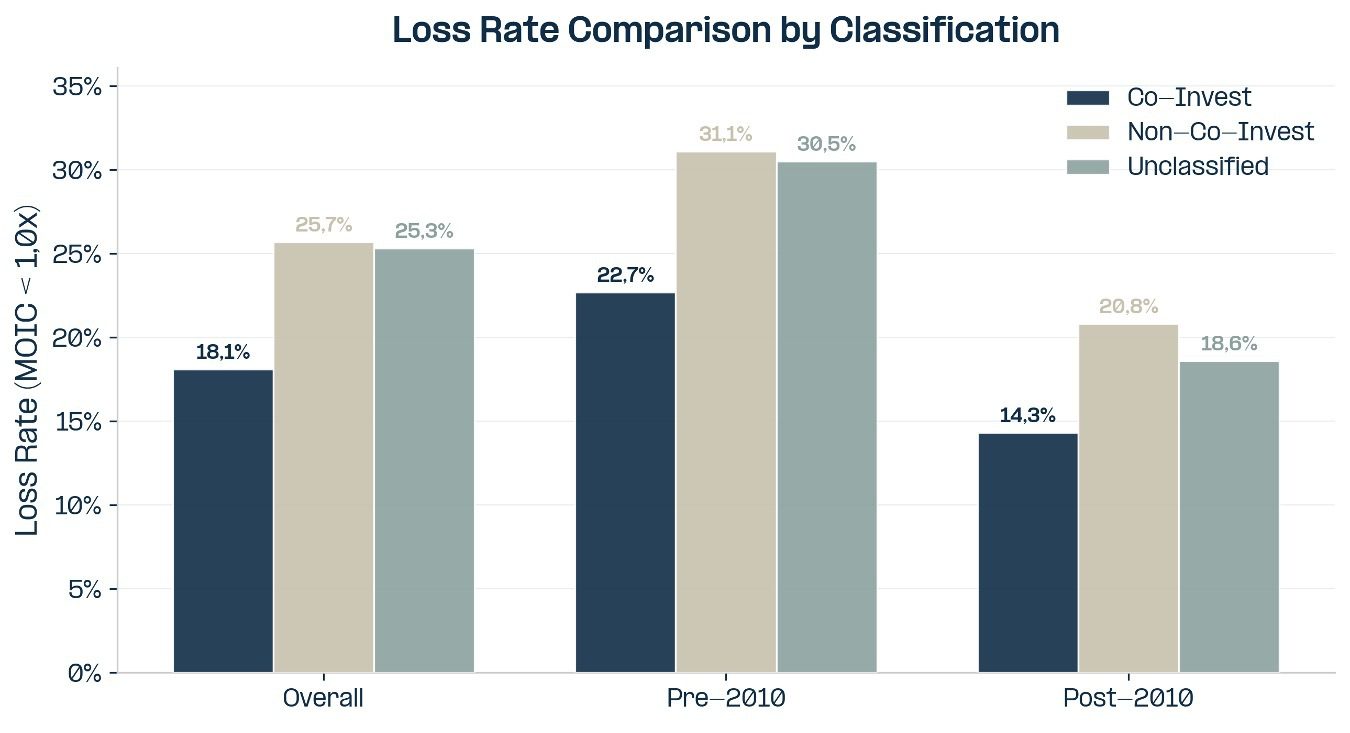

The loss rate advantage is not limited to older vintages. In the post-2010 era, co-investments still exhibit lower loss rates: 14.3% versus 20.8% for non-co-investments. While the smaller sample of recent realized deals limits statistical power, the directional pattern is consistent with the full-sample finding. The co-investment downside advantage persists across every sub-period we tested.

Figure 1: Return distributions for the three groups. Co-investments show a rightward shift and a thinner left tail.

Higher returns on co-investment deals

Co-investments returned more and lost less. But could this simply reflect differences in deal characteristics rather than co-investment status itself?

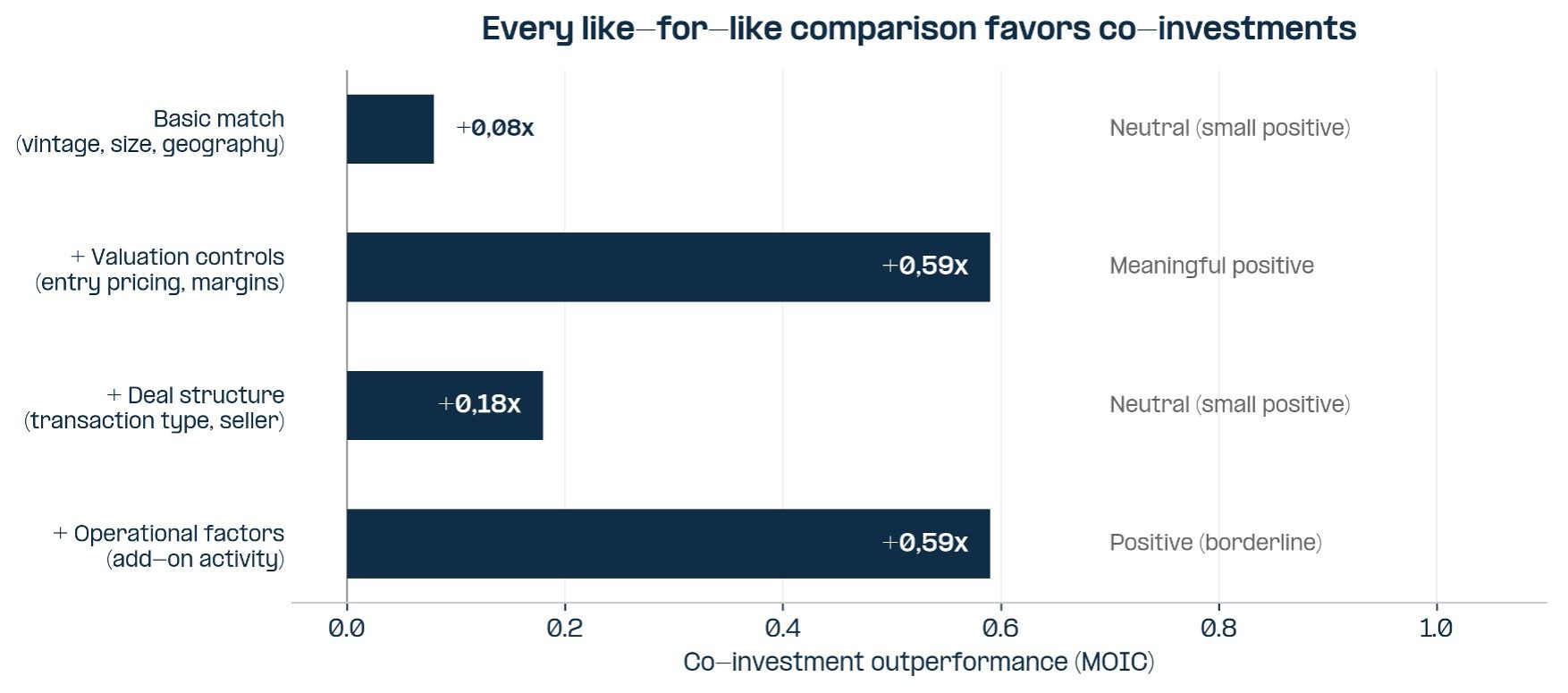

To answer that, we ran a series of like-for-like comparisons. Each co-investment was matched to a similar fund-only deal based on vintage year, deal size and geography. We then progressively added stricter controls (entry valuation, deal structure and operational characteristics) to see whether the results held up to isolate the co-investment effect from differences in deal mix.

| Comparison | What we controlled for | Result |

| Basic match | Vintage, size, geography | Neutral (small positive) |

| + Valuation controls | + entry pricing, margins | Meaningful positive |

| + Deal structure | + transaction type, seller | Neutral (small positive) |

| + Operational factors | + add-on activity | Positive (borderline) |

A positive result means co-investments outperformed matched fund-only deals; neutral means no meaningful difference. None of the four comparisons showed co-investment underperformance. See white paper for details on within-manager co-investment performance.

Across all four increasingly strict comparisons, co-investments performed at or above matched fund-only deals. None showed underperformance. The evidence is consistent with GPs offering their highest-conviction deals to co-investment partners. Within individual GP portfolios, the pattern holds: the majority of managers produced higher returns on their co-investment deals than on their fund-only deals.

Figure 2: Every like-for-like comparison favors co-investments. None shows underperformance. Bars show how much co-investments outperformed matched fund-only deals.

Entry discipline matters

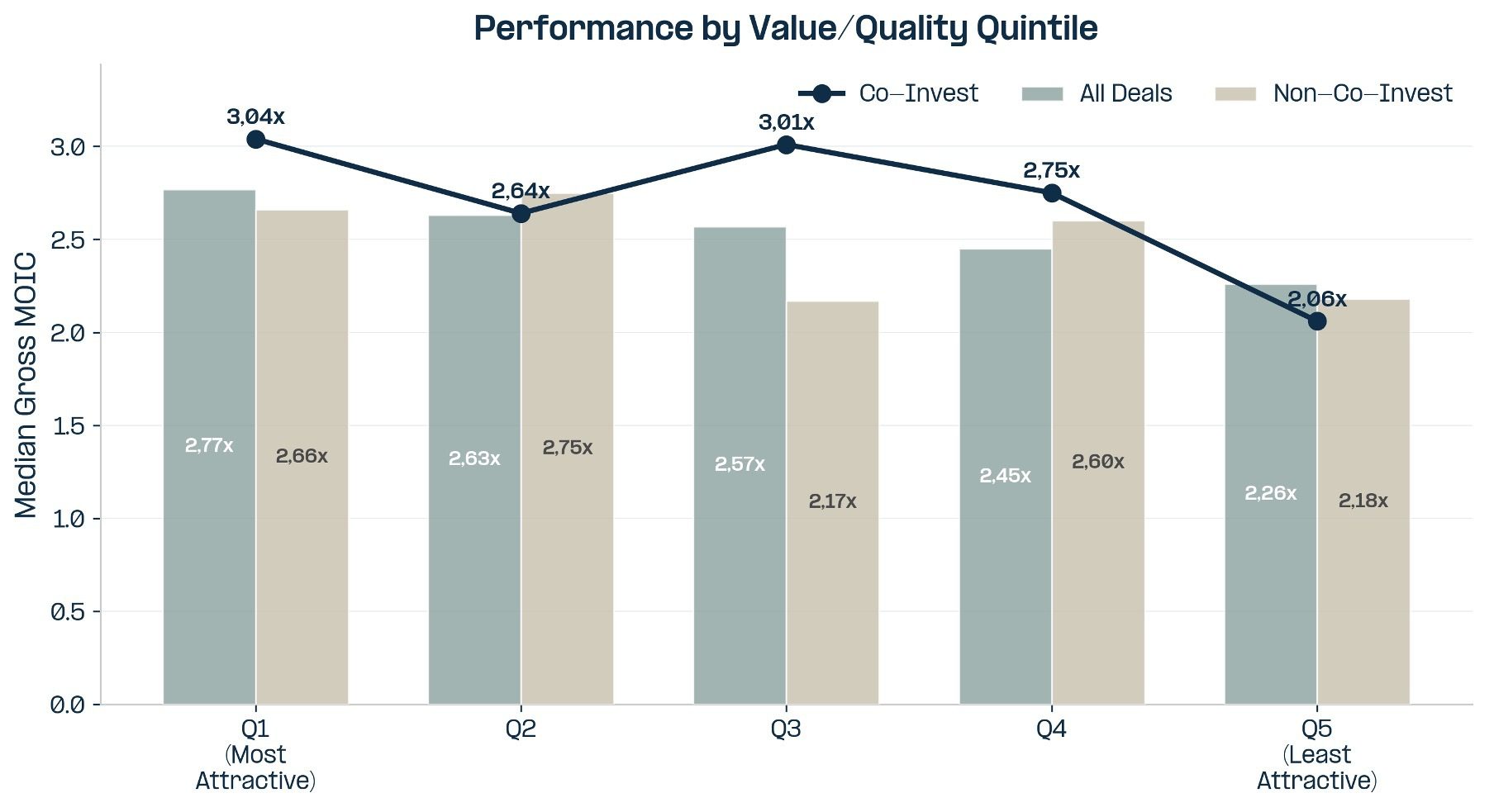

However, not all co-investments perform equally. A ranking based on entry characteristics (company size, entry valuation and profitability) reveals that deal selection matters at least as much as co-investment status.

The spread from Q1 to Q5 is nearly 1.0x for co-investments but only about 0.5x for non-co-investments. In a co-investment, the LP takes concentrated single-deal exposure rather than having outcomes diluted across a diversified fund. Overpaying therefore has a more direct impact on returns.

Figure 3: Median MOIC by value/quality quintile. The gradient from Q1 to Q5 is steepest for co-investments.

The pattern also holds in the middle of the distribution: Q3 co-investments outperformed Q3 non-co-investments by a wide margin, while Q4 co-investments still outpaced their non-co-investment counterparts. This shows that entry discipline matters throughout, not only at the extremes.

These are factors observable at the time of investment. Active deal selection – the ability to evaluate entry pricing, business quality and deal structure independently – is a meaningful part of co-investment program design.

What this means in practice

Based on our research, there are a few practical implications for investors evaluating or building a co-investment program:

- Co-investment deal quality is robust. Across every analytical cut in this study, co-investments perform at least in line with fund-only deals, gross of total fees, and typically better. The concern that GPs use co-investment to offload weaker deals finds no support in our data. For allocators evaluating whether to build or expand a co-investment program, the quality-of-deal-flow question should not be the barrier.

- Downside protection is real. Co-investments lose money less often: roughly 18% versus 26%. For a 50-deal portfolio, that translates to approximately four fewer losses.

Figure 4: Co-investments consistently exhibit lower loss rates across geographies and time periods.

- Entry discipline is the differentiator. Active deal selection, entry pricing discipline and deep GP relationships are the factors that separate strong co-investment outcomes from average ones.

At Evli, these principles are embedded in how we evaluate and execute co-investments alongside our GP partners.

For the full methodology, detailed results and additional analyses including geographic return differences, vintage period dynamics, entry quality quintile rankings, within-manager confirmation and unrealized portfolio confirmation, read our white paper “Co-Investments in Private Equity: Lemons or Gems? Evidence from 8,200 Deals”.

White paper: Co-Investments in Private Equity: Lemons or Gems?

Co-investment has moved from a niche arrangement for the largest institutional investors to a mainstream allocation strategy. Around $33 billion was raised across co-investment vehicles in 2024. The appeal comes with a persistent question: are GPs offering their best deals, or their worst?

Interested in alternative investments? Further reading:

Evli’s co-investment strategy: opening the door to direct private equity deals

The contents of this article should not be considered as investment advice and should not be relied upon in making an investment decision. Before making an investment decision, please consult the fund's legal documents, such as the key investor document. The information is available to those considering an investment from Evli. Historical returns are no guarantee of future returns. The value of an investment may rise and fall and the investor may lose some or all of the capital invested.