The United States and Israel launched joint airstrikes on Iran at the end of February, resulting in the death of the country’s Supreme Leader, Ayatollah Ali Khamenei, and other senior officials. Iran responded by striking targets in neighboring countries and by closing the Strait of Hormuz, a critical route for global oil supplies. Brent crude oil rose above USD 85 per barrel, and the equity markets reacted negatively. The volatile situation is having a negative impact on the global economic outlook. Much depends on how long the crisis lasts.

Earlier in February, manufacturing PMIs in the US and Asia improved, while economic growth in the euro area exceeded expectations. In Germany, fiscal stimulus is expected to strengthen the economic outlook. Continued global investment in AI is expected to support both the industrial and technology sectors. In the US, the unemployment rate fell to 4.3 percent, and job growth remained strong. Inflation slowed to 2.4 percent, reinforcing expectations of future rate cuts. However, the mixed economic picture – strong employment but soft retail sales – is likely to keep the Fed cautious.

Inflation in Europe eased significantly. In France, inflation is at its lowest level in five years, while euro-area inflation stands at 1.7 percent. In Germany, inflation increased slightly but is expected to remain moderate. In the euro area, a stronger euro is adding to deflationary pressures and could raise the likelihood of a rate cut later this year.

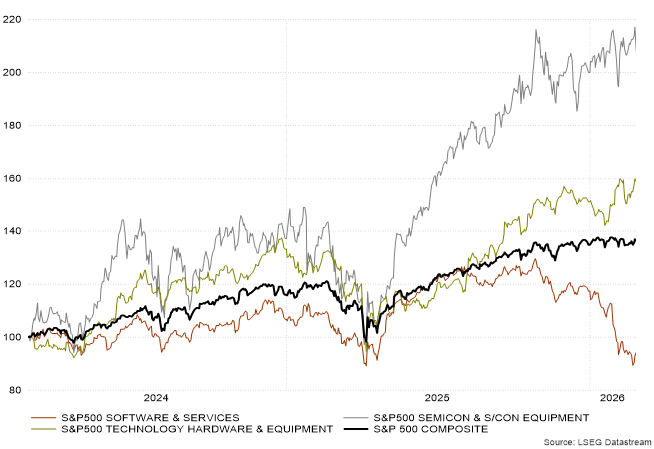

US earnings growth strong, but markets remain flat

The US earnings season got off to a strong start, with corporate profits in the final quarter of 2025 rising nearly 15 percent, exceeding analysts’ expectations. Meta delivered a positive surprise, driven by AI-related advertising revenue, while Microsoft’s weaker-than-expected cloud guidance weighed on its equities. Markets showed growing concern over rising component costs, data center power constraints, margin pressures, and the broader impact of AI across industries. Equity markets displayed a clear rotation: software equities declined sharply as new AI models prompted questions about their long-term competitiveness. The MSCI North America Index closed February unchanged.

AI spurs growth in semiconductor market

Investment in AI has reached historical levels: Alphabet, Meta and Amazon plan to invest more than USD 500 billion in AI infrastructure, far exceeding consensus forecasts. This is expected to sustain strong demand for semiconductors and support growth in the sector. In emerging markets, return expectations remain strong. Taiwan and South Korea, for example, stand to benefit from the semiconductor sector and its robust fundamentals. Korea’s Kospi Index rose more than 20 percent in euro terms in February. The MSCI China Index fell by nearly six percent, but the MSCI Emerging Markets Index still gained more than six percent over the month. Japanese equities rallied strongly, with the MSCI Japan Index finishing more than seven percent higher in euro terms. The Japanese yen has depreciated roughly 18 percent against the euro over the past year.

Earnings growth in Europe is expected to remain below five percent. Analysts have slightly revised down their forecasts, but an improvement in earnings remains possible, largely dependent on a pick-up in economic growth. The industrial sector maintained strong performance, supported by growth in the defense industry and rising demand for data center solutions related to AI. The MSCI Europe Index gained approximately four percent. Value equities and defensive sectors outperformed the broader market.

SCOTUS, POTUS and US tariffs

The Supreme Court of the United States (SCOTUS) ruled that the IEEPA emergency tariffs previously imposed by the US President (POTUS) were illegal. However, the temporary general tariff that replaces them keeps the effective rate nearly unchanged. The ruling is not expected to materially alter the inflation or growth outlook. However, uncertainty around global trade terms has risen again. The Trump administration is seeking ways to maintain the tariffs.

In February, gold saw its largest daily decline in decades following a sharp rise in January. Silver followed a similar pattern, while the US dollar strengthened significantly. Gold recovered to over USD 5,000 per ounce during February, approaching the January peak. Long-term interest rates declined significantly by 0.25 percentage points in the United States and by 0.17 percentage points in Germany.

Figure: Software equities decline amid AI-related concerns