The European High Yield market is attractive to investors who want to add variety to their investments and aim for higher returns. To make smart investment choices, it's important to understand this market, especially how the bond spread, and cash prices presently are valued. Here's a quick overview of the current EHY market.

European High Yield Spread: Close to the 10-Year Average

A bond's yield spread is the gap between its yield and the yield of a risk-free bond (usually a government bond). This spread shows the extra risk an investor takes when investing in a high-yield bond instead of a risk-free one.

Right now, the European High Yield (EHY) spread is around its 10-year average. This suggests that the market's view of risk in the EHY sector is neither too positive nor too negative, but rather in line with past trends. Basically, the market sees the risk of EHY bonds as consistent with the last ten years. This could be seen as a sign of relative stability, especially considering the economic turmoil and uncertainties we've experienced in the past decade.

The Appeal of Bond Cash Prices

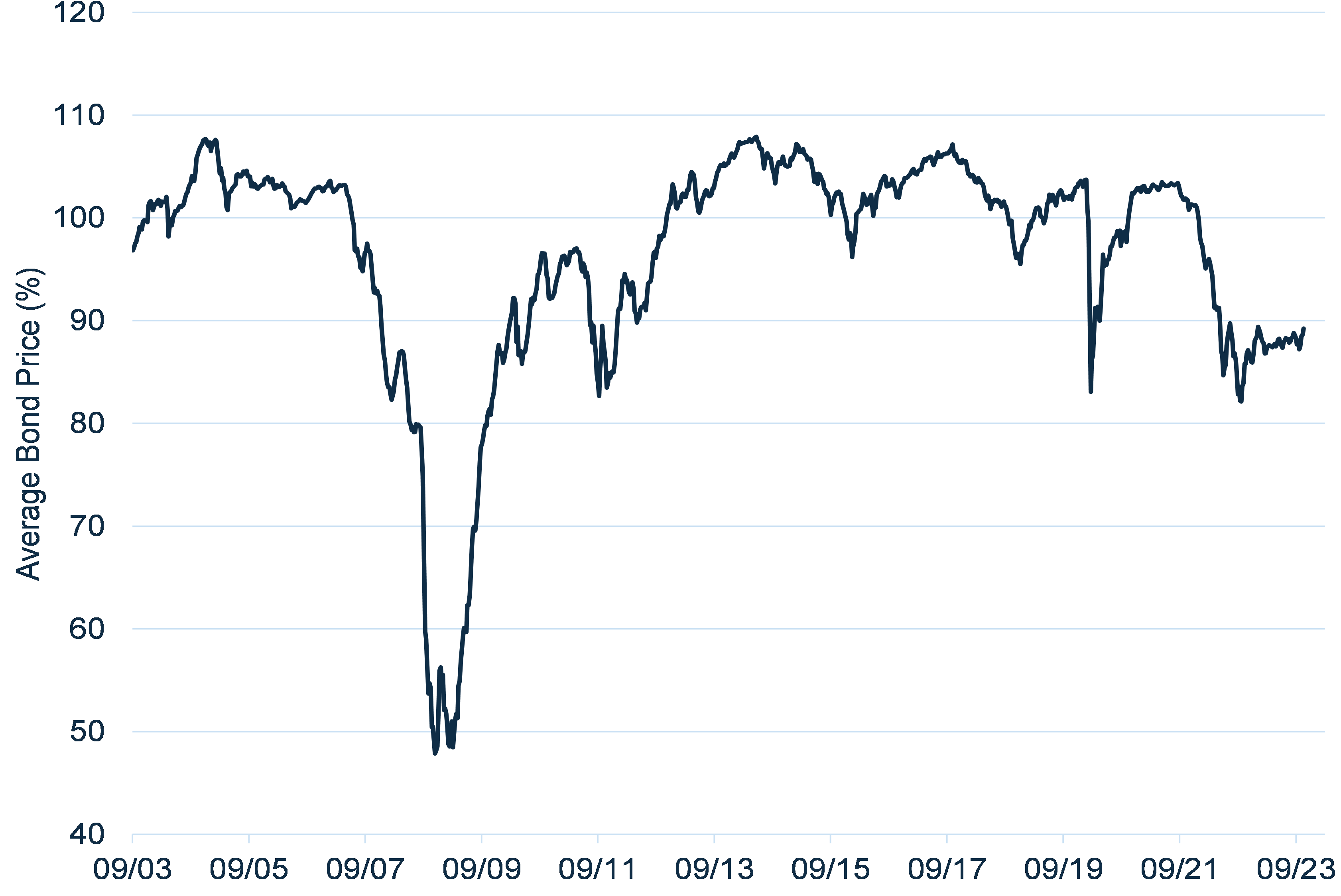

While the spread is at its historical average, the actual cash prices of these bonds are quite attractive. Why? Because of rising interest rates during 2022.

When interest rates go up, bond prices go down. This is because new bonds issued at the current higher interest rates make older bonds with lower rates less appealing. So, to compete with new issues, the prices of older bonds have to drop.

This situation is a great opportunity for investors looking to invest in the EHY market. Presently, the markets yield to maturity is over 8%, clearly the highest it has been in over 10 years. Also, the discount seen in bond prices is at a level usually seen when default levels are very high. But currently, default levels are really low and company performances have been strong.

Average Bond Prices at levels usually seen in a crisis

Source: ICE, Index: ICE BofA European Currency Developed High Yield Constrained Index

Why It's Important

Often, bond documents allow the company to pay back the bonds early. The initial repayment dates are at a premium, or above 100, but as maturity nears, the price drops to 100. For instance, a 7-year bond typically allows the issuer to repay the bonds 2 years before maturity. If we consider a bond with average High Yield market characteristics; 4 years to maturity, price is 88, coupon 4.3%, that bond would have a Yield-to-Maturity of 7.92%. But if the company repays it 1 year before maturity, the YTM increases by 112 bps to 9.04%, and if repaid 2 years earlier, the yield would rise by a massive 342 bps to 11.34%. This clearly shows huge potential for higher returns. However, not every company will repay the bonds that early, as refinancing depends on factors like the coupon on the old bonds, recent results, market conditions, etc. But the potential for additional yield not reflected in the headline spread and yield numbers is substantial. In the high-yield markets, it's very common for refinancing to occur before maturity, even when the new interest rate is higher. This is because companies aim to reduce refinancing risk and therefore prefer to repay the bonds earlier than the final maturity date.

Wrapping Up

In short, while the Euro High Yield spread is reassuring at its current levels, the bond prices, hurt by rising interest rates, offer investors potential for extra returns that are not visible by just looking at spread graphs. Feel free to contact us for detailed information and advice customized for your specific needs and investment goals.