We have always been excited about investing in emerging markets. Not everyone has shared our conviction, but now EM’s future seems so bright that we can’t resist providing our thoughts on why EM is positioned to outperform in the next several years.

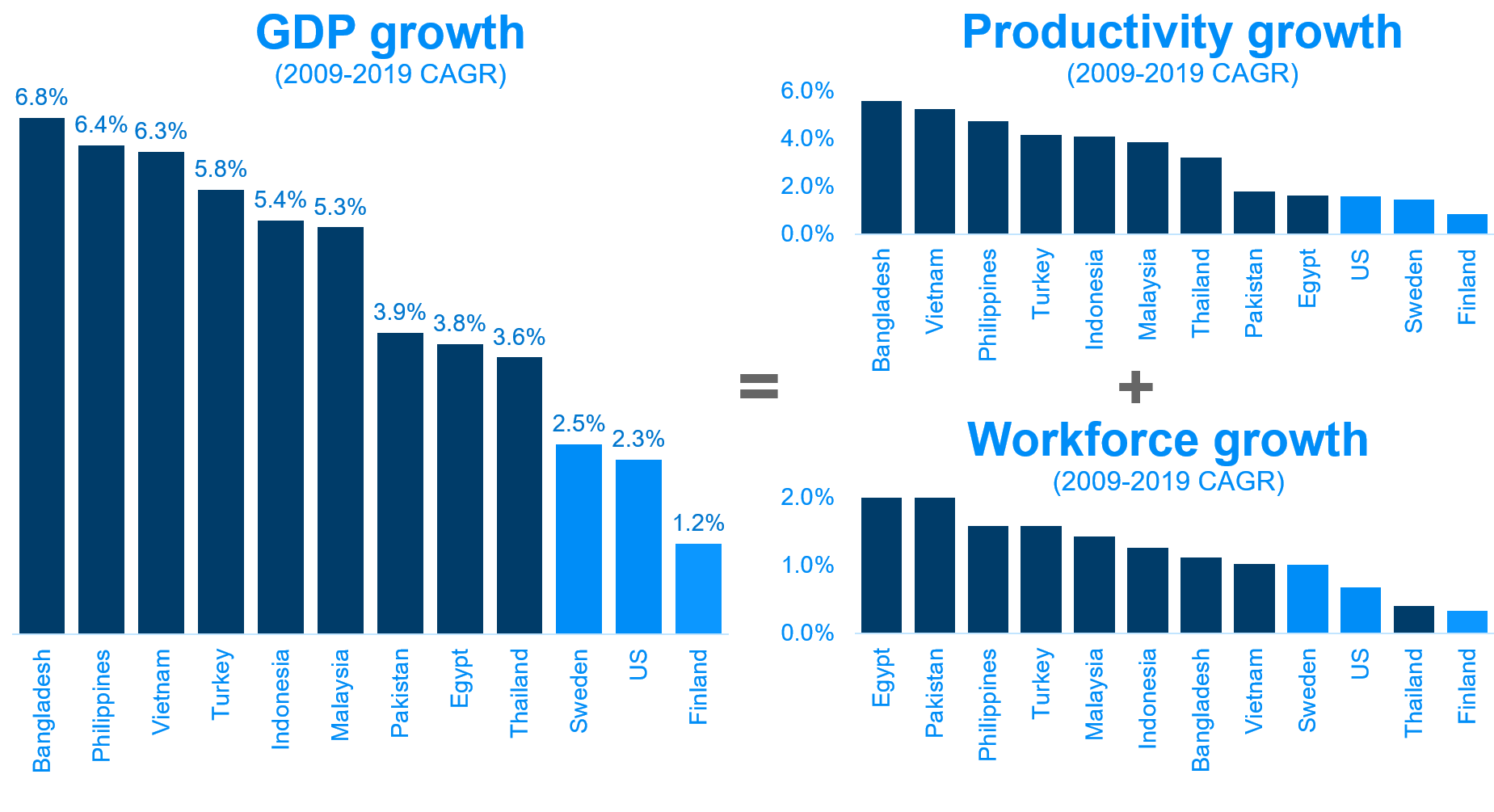

Productivity gains and the demographic dividend

The long-term EM story is familiar to most investors: these markets grow much faster than developed economies. This is a function of more impressive productivity gains as there is greater room for improvement, and higher workforce growth as the working-age population is expanding in most emerging markets while it is shrinking in the developed world. Investors in emerging markets can capture this extra growth through the expanding corporate earnings of publicly listed companies.

Source: World Bank.

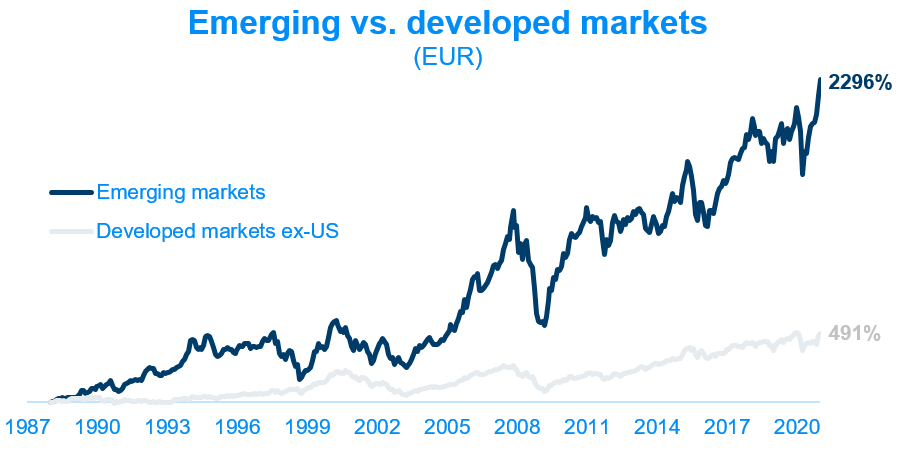

Long-run EM outperformance

The patient investor has been rewarded for investing in emerging markets over the long run. In the last 30 years, EM has outperformed developed markets by a factor of 4x. But this is simply passive investing. An astute active investor should get rewarded with even higher returns given that emerging markets are less efficient than developed markets and thus provide compelling opportunities to find undiscovered companies as well as to unlock shareholder value through friendly activist engagement.

Source: Bloomberg.

Note: Indexes used are MSCI Emerging Markets and MSCI World ex-US. Returns prior to 1999 are in USD.

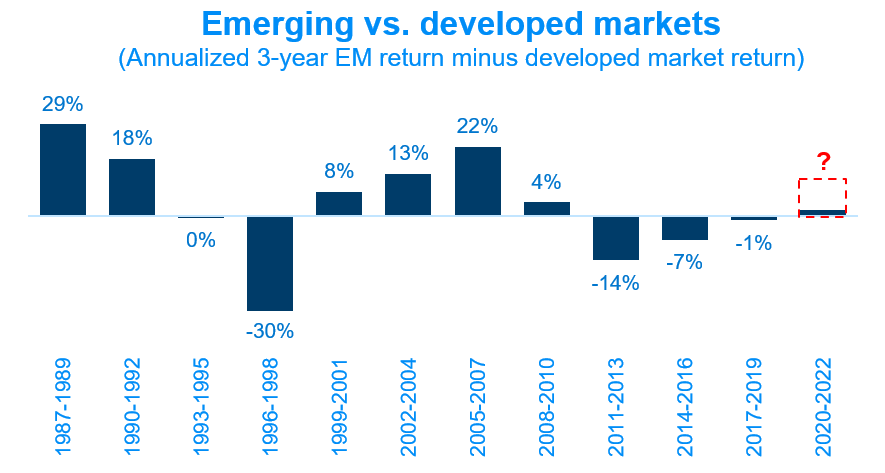

Cyclicality of EM/DM performance

Long-term performance of EM equities relative to that of developed markets equities seems to work in cycles. The past decade favored developed markets. Might we be coming out of a long cycle of EM underperformance and entering a long cycle of EM outperformance?

Source: Bloomberg.

Note: Indexes used are MSCI Emerging Markets and MSCI World.

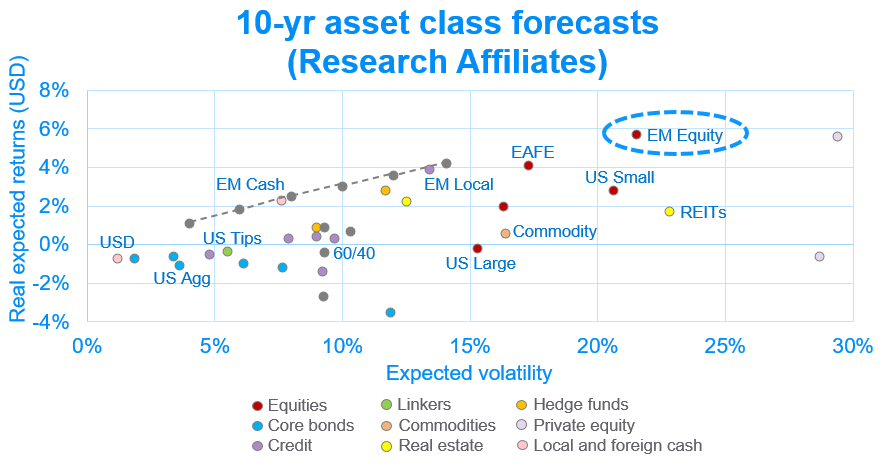

Long-term asset class forecast

Two global asset allocators with a history of making successful predictions of long-term future asset class performance, GMO and Research Affiliates, both forecast emerging markets equities to outperform all other asset classes in the next 7 and 10 years respectively. Given our focus on value, of particular excitement to our investors should be GMO’s prognosis that EM value equities will outperform the rest of EM.

Source: Research Affiliates.

Source: GMO.

Drivers of outperformance

We believe there are four main drivers behind the forecasted emerging markets outperformance: 1) recovery of the commodities supercycle, 2) a weakening US dollar, 3) attractive valuations, and 4) EM inflows due to increased allocation by institutional investors.

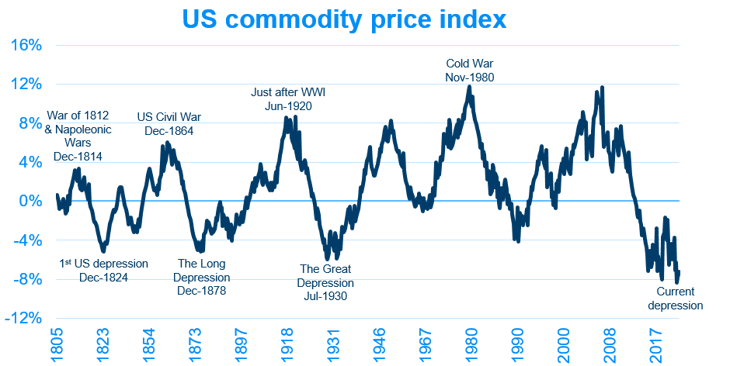

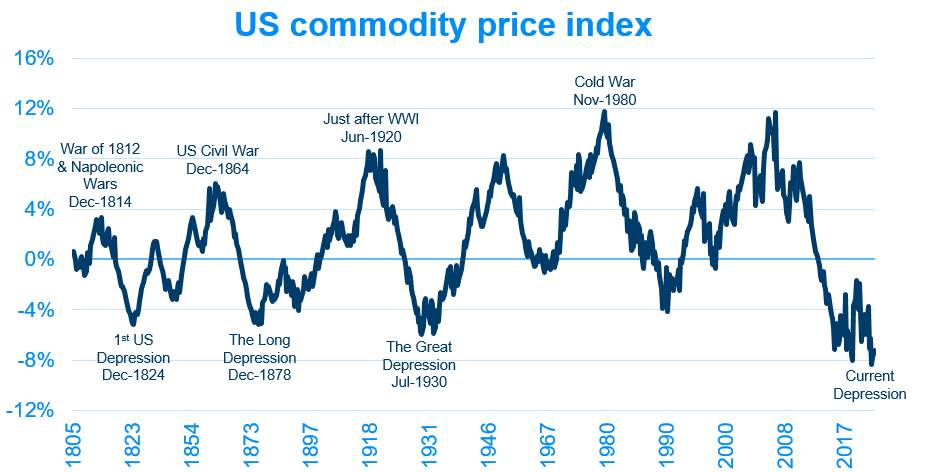

1. Recovery of the commodities supercycle

It is widely known that EM is strongly correlated with commodities given that many emerging markets depend on exports of their natural resources. It is also widely accepted that commodities markets move in decades-long supercycles. With every single commodity except for wheat in deficit today, and with structural under-investment in supply, we appear to be late in the supercycle and the commodities bull market might lie shortly ahead.

Adding support to the commodities bull-market thesis is the fact that inflation expectations may start to edge higher due to the enormous global stimulus – both expansionary fiscal policy and rising money supply – in response to the demand shock caused by the COVID-19 pandemic.

Furthermore, demand from China is a significant driver of metals prices. The People’s Bank of China’s recent rate cuts, along with the continued growth in the government’s infrastructure spending, and recent policy shifts benefiting the auto and housing industries should provide catalysts to the reflation of commodities.

The long-expected energy transition is unlikely to impact the commodities supercycle at this time due to the supply limitations in the global lithium market, which slows down the development of battery technologies necessary for mass adoption of electric vehicles.

Source: Stifel Report June 2020.

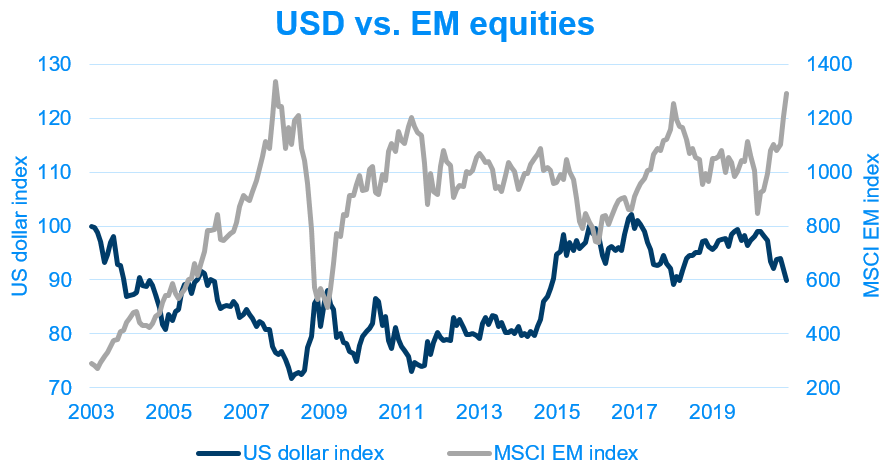

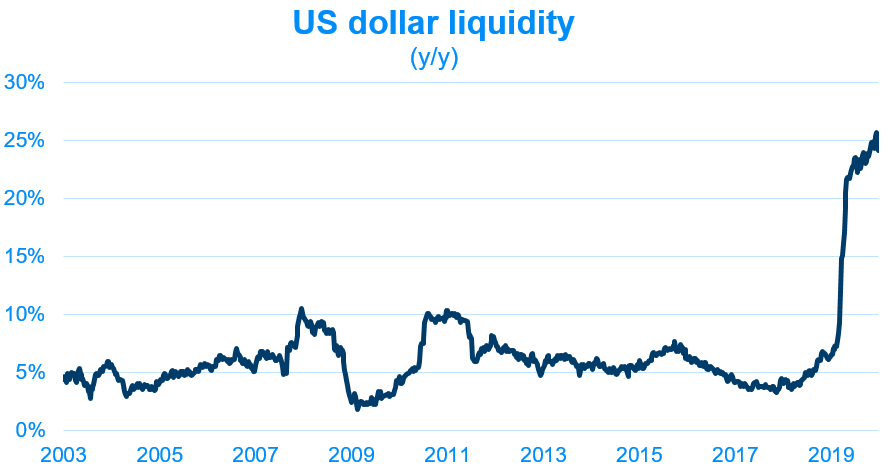

2. A weakening US dollar driven by low rates and record liquidity

There is a strongly documented inverse relationship between the strength of the US dollar and emerging markets equity performance. Whenever the dollar goes into a cycle of weakness, EM equities outperform.

Ultra-low interest rates in the US – until recently the only large developed market to have offered attractive risk-adjusted returns – have brought US investment yields to the ground. Investors looking for alternative locations to find yield are turning to emerging markets, a rare asset class where high yields can still be found, resulting in less demand for the US dollar as investors sell dollars to buy other currencies.

Additionally, global US dollar liquidity has risen over the past year at the fastest pace ever recorded due to the extraordinary policies implemented by the Fed and other central banks. An increase in US money supply, particularly at times of low growth and large fiscal and current account deficits, tends to be associated with a weak dollar and benefits emerging markets.

A weak dollar also makes it easier for EM countries to repay their dollar-denominated debt and focus on increasing domestic investment and fiscal stimulus programs, boosting economic growth. Commodity importers benefit from the dollar-denominated commodity prices as their currencies strengthen against the dollar, while commodity exporters benefit from the increased demand for commodities.

Source: Bloomberg.

Source: Bloomberg.

Source: Bloomberg, Federal Reserve, and US Treasury.

Note: US dollar liquidity is measured as US money supply (M2) plus US total international reserves.

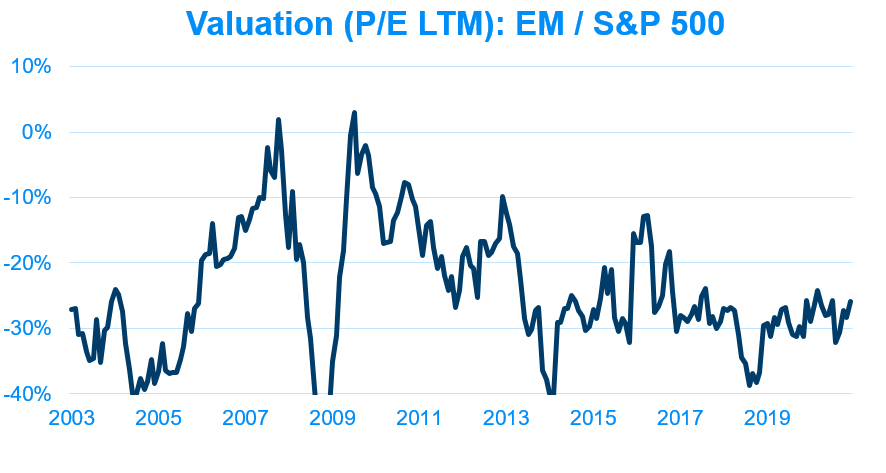

3. Attractive valuations

The low risk-free yields in the US have pushed US risky assets to high valuations which keep investors up at night as they might leave little room for continued expansion and plenty of downside. Indeed, stock market valuations in the US are higher than at any other time in history except for just prior to the tech bubble. These valuations would be especially unwarranted if increases in raw material commodities prices start eating into corporate earnings.

On the other hand, emerging markets’ strong growth comes significantly cheaper. Just as at the beginning of the last emerging markets bull market nearly two decades ago, the valuation of EM companies relative to developed markets’ appears attractive.

Source: Bloomberg.

Source: Bloomberg.

Note: LTM earnings used in the calculation of P/Es in 2020 are normalized using December 2019 LTM earnings in order to normalize COVID-19 impact on earnings.

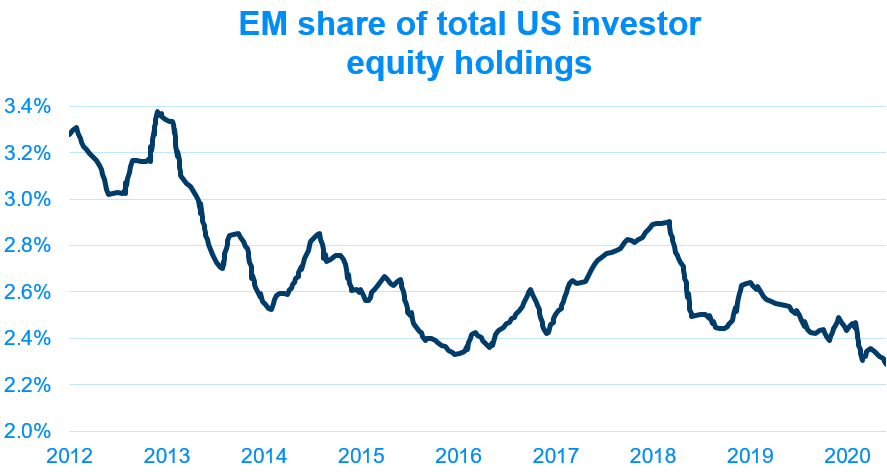

4. EM inflows due to increased allocation by institutional investors

After a decade of US equity dominance, institutional investors have record-low allocations to EM equities. Flows to EM only turned positive during the last few months of 2020 and seem to be accelerating. From such a low base, it is easy to see a scenario in which institutional investors reallocate massively to EM. Such fund flows would most certainly push up prices broadly across emerging markets, creating a sort of self-fulfilling prophecy for investors who believe now is the time for emerging markets to outperform.

Source: Exante Data, Federal Reserve.

Conclusion

The relatively faster gains in productivity and favorable demographic backdrop are the long-term drivers for EM. However, macro cycles make EM particularly more attractive at certain times, and we are convinced now is one of those times. This conviction is supported by where we are in the commodities cycle, the low yields in developed economies and a spike in US dollar liquidity leading to a weakening dollar, cheap valuations in EM relative to developed markets, and institutional investors’ ability to push massive flows into emerging markets.

It’s time for EM to take the reins.

Learn more about our Evli Emerging Frontier Fund

Our recent blogs

Testing our portfolio for COVID-19: Why we sold Turkey

The value of investor meetings: Five things we learned from interviewing 323 CEOs last year

+1,000% during COVID-19: Protecting our portfolio with Malaysian medical gloves

A month in Turkey: Retreating from coronavirus

A month in South Africa: The road to nowhere

A month in Saudi Arabia: Piercing the veil

A month in Vietnam: Closing the deal

A month in Thailand: Driving three hours to see an empty factory

A month in Pakistan: An altercation at the ministry of finance

A month in Bangladesh: We're investing billions in the world’s best stock market

A month in Indonesia: Offending Trump in Bali

A month in Malaysia: Finding another gem on "Treasure Island"

A month in the Philippines: How active management helped us beat the traffic (and the market)